|

This

example comes from a book Introduction to Stochastic Programming by

Sheldon M. Ross, (Academic Press, 1982). In the book the problem

is described with a continuous nonnegative state unbounded

from above. The action variable is also continuous. For our

purposes we will discretize both state and action.

A gambler is playing a game that

has two results, win or lose. He can bet any amount up

to his entire wealth. If he wins the amount of the bet

is added to his wealth, and if he loses the amount of

the bet is subtracted from his wealth. The gambler's

goal is to maximize the log of his wealth after a fixed

number of plays. |

To make analysis possible, we define the gambler's wealth

as the state variable measured in whole dollars. We restrict

the gambler's wealth to be less than the quantity M.

Bets are measured in dollars and in this model the

amount of the bet is the action variable. Bets

are restricted so that the gambler can never bet an amount

that would reduce his wealth to less than $1 or more than M.

There are N plays in the game and the objective is

to maximize the log of the wealth after play N.

|

States |

| |

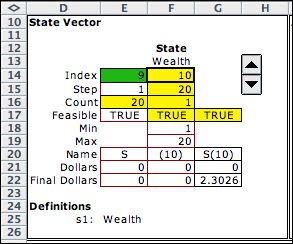

The states are defined

with a single state variable. The

state definition region on the model worksheet is shown below.

Cell F14 holds the value of the current state, 10. For the

example we choose to limit the wealth to $20. The lower bound

on the state is in F18, and the upper bound is in F19.

The example illustrates a new feature of the DP

Models add-in, the ability to define the values for the final

state. This is important for finite time horizon problems. For

the Gambler problem, the only objective concerns the value at

the final state. The goal is to maximize the log of the wealth

at the end of the time horizon, 20 plays for the example shown

above.

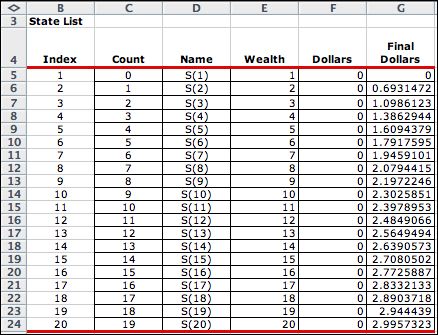

After enumeration the state list appears as below.

The Final Dollars column is computed as ln(final wealth).

|

Actions |

| |

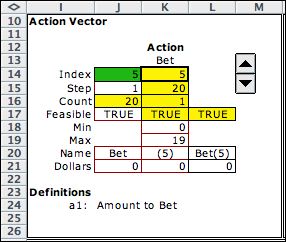

The action is the

amount the gambler bets on a given play. The range of bets is

defined in the action element. The goal of the DP is to select

bets at each state to maximize the log of the wealth at the end

of the game. |

|

|

Events |

| |

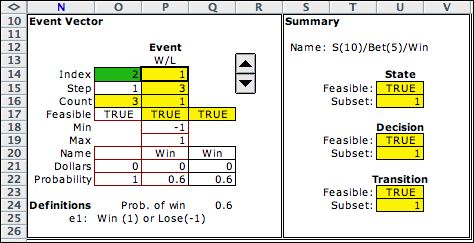

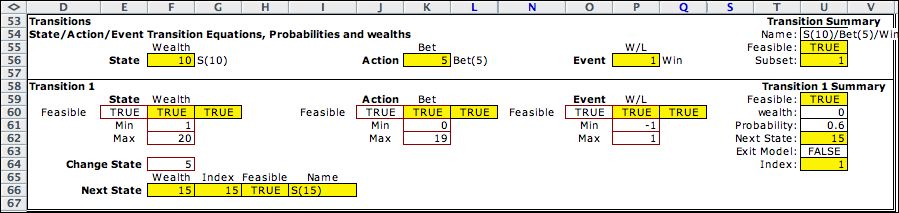

The event indicates whether

the bet wins or loses. The probability of winning is a parameter

of the system, stored in Q24. The example assumes the probability

of winning is 0.6 with a corresponding probability of losing

of 0.4. The summary starting in column S shows that the combination

of elements, S(10)/Bet(5)/Win, is feasible. |

|

Decisions |

| |

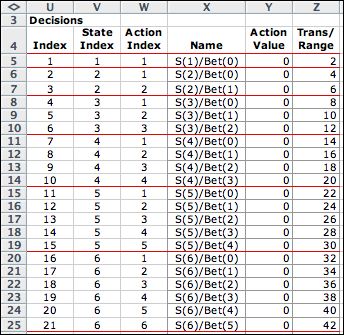

Not all combinations

of state and action are admissible. We reject all actions that

might lead to a state less than 1 or more than 20. This is accomplished

in the single decision block of the model. The Max entry

in column K holds a formula that limits the size of the bet.

The maximum bet with a wealth of 10 is a bet of 9. any larger

bet allows the possibility that the wealth falls below 1 or above

20. |

|

| |

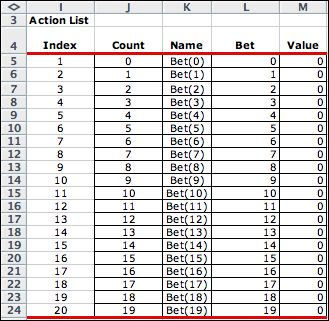

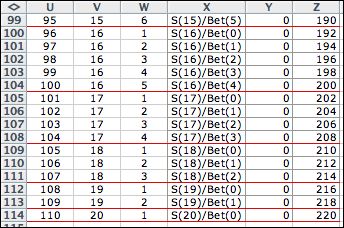

Enumeration of the elements

reveals that there are 110 feasible combinations of state and

action. Near the top of the list the actions are limited by the

risk of falling below 1. Near the bottom of the list the actions

are limited by the possibility of falling above the maximum wealth

of 20. |

| |

.

|

Transitions |

| |

The transition equation

is particularly simple for this model. The change state cell,

F64, contains a formula that evaluates the positive of the bet

for a win event, and evaluates as the negative of the bet for

the lose event. The example shows that betting 5 when the wealth is

10 increases the wealth to 15 because of the win event. |

|

| |

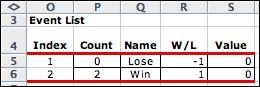

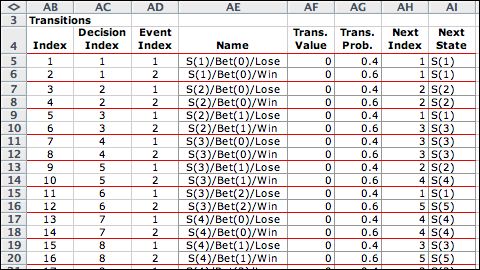

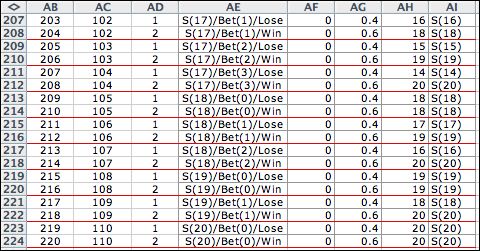

There are two events

for every decision so the transition list has 220 entries. |

| |

.

|

| |

The gambler problem is

solved on the next page. |

| |

|