|

We illustrate the analysis of

the example using screen shots from the Stochastic

Analysis Excel add-in. We model the ATM machine system

as a continuous time Markov Chain. The CTMC section

in the Computations section describes how to use the add-in

for this example.

The example used here is very simple, but very complex systems

can be analyzed with these techniques. |

|

| |

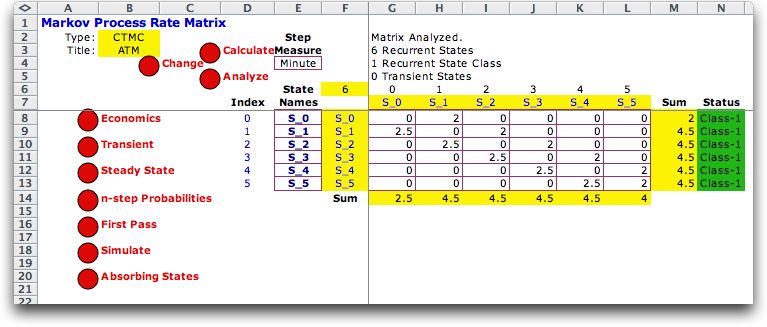

The CTMC model is defined by the

rate matrix. There are six states indicating the number of

customers in the system, from S0 through S5. When the system

is empty (S0), the only event that can occur is for an arrival

to occur. This occurs at the rate of 2 per minute. The rate

is placed on the (0,1) element of the matrix indicating that

the transition moves the system from S0 to S1. No other transitions

are possible, so all other entries in the S0 row are zero.

We are indexing the matrix from 0 to 5 to correspond to the

state definitions.

When one customer is in the system, two events can occur.

An arrival leads the system to S2, as indicated by the rate

2 in element (1,2). With a service completion, a customer leaves

the system and the system is in S1. The rate of service is

2.5 per minute. This number is placed in element (1,0).

The rows for states 2 through 4 are constructed

similarly. For S5, the system is full and an arriving customer

does enter. We represent that possibility with the rate 2 in

element (5,5). It

is actually unimportant whether we put 0 or 2 in element (5,5). |

|

| |

The rate matrix is the primary

model component for the CTMC. Note that the rows do not sum

to 1 as do the row sums for the DTMC because the numbers in

the matrix are not probabilities. They are rates. The assumption

of the CTMC is that all transitions are governed by exponential

distributions with parameters given in the rate matrix.

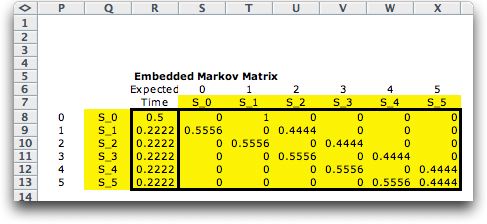

The rate matrix determines a second matrix called the Embedded

DTMC Matrix. This is the DTMC that describes the steps

of the process. A step occurs each time the process changes

from one state to another. The times between steps have exponential

distributions.

Many of the results of CTMC can be described in terms of both

time and steps. We use the embedded DTMC to determine

the classification of the states. For the ATM example all the

states are all recurrent. |

|

Economics |

| |

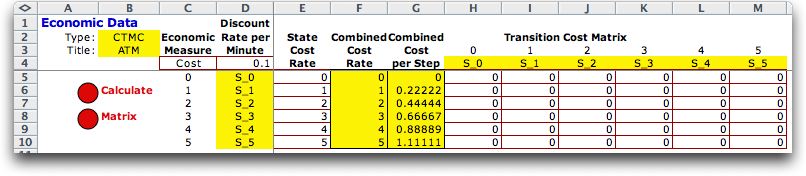

The cost data is entered on the Economics worksheet.

There are two kinds of costs. The state cost is incurred during

the time the process is in a state, and the transition cost

is incurred when the process moves from one state to another.

State costs are given as rates per unit time. The discount

rate is for time value of money computations and continuous

compounding is assumed. The transition cost matrix is similar

to the one used for CTMC.

For the example, we assign a cost rate of 1 per minute

for each customer in the system. For example with five customers

in the system, cost is assigned to the system at the rate of

5 per minute. |

| |

|

Transient Analysis |

| |

The transient analysis describes

the process in steps of the embedded DTMC. An initial

state is defined in the top row of the state display. Subsequent

calculations give state probabilities for each of the first

20 steps. Columns to the right of the state probabilities show

expected time and cost

calculations.

Since the time between each sequential pair of steps is a

random variable with known probability distribution, we

compute the expected time for an event to occur. For example,

we see that the first step will surely lead from S0 to S1.

The expected time for the step is 0.5 minutes. The subsequent

computations are not easy to explain, but we see that after

20 steps, the system is expected to be almost 6 minutes into

operation. Columns in the display show the cost rates (per

minute) and the net present worth (NPW) computed with continuous

compounding.

Clicking the More button gives 20 additional

days. The Start button allows a different selection

of the initial state. |

| |

|

| |

The Chart button creates are

graph of the transient probabilities. Note that the axis of the

graph is steps rather than time. |

| |

|

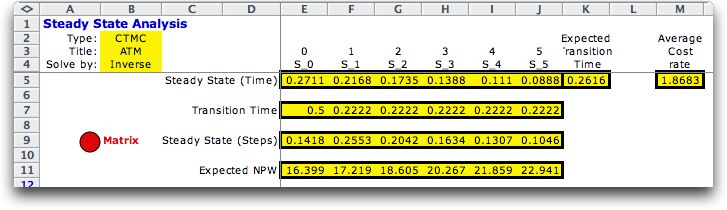

Steady-State Analysis |

| |

For the CTMC there are two kinds

of steady state probabilities. The time-state probability for

a given state is the probability that the system will be found

in that state at a randomly selected time. If the time is remote

from the starting time, the probability becomes independent

of the initial state and converges with time to the time-steady-state

probability. The first colored row (row 5) shows these

probabilities for each state.

Whenever the system is in a given state, there is an expected

time before the system will leave the state. These results

are reported in row 7. Multiplying rows 5 and 7 together, we

find the expected transition time at steady state in cell K5.

A useful result is the Average Cost Rate (M5) that comes

from the combination of the time-steady-state

probabilities and the economic parameters.

An analysis of the embedded DTMC provides the step-steady-state probabilities.

The steady state probability for state j is

the limiting probability that the process is in state j after

a large number of steps.

The analysis also provides the expected NPW as a function

of the starting state. Most steady state results are independent

of the starting state, but the NPW weighs early events more

heavily than later ones, so the initial state does make a difference.

|

n-Step Probabilities |

| |

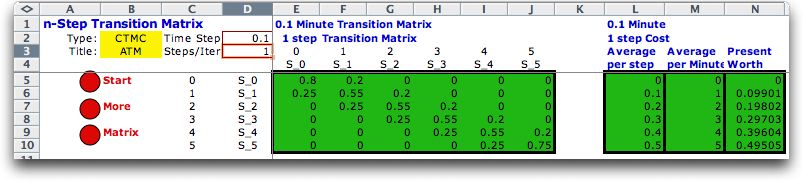

These results are obtained by

discretizing time with a given step size. Cell D2 holds the

time-step size of 0.1 minute for the example. Using this time,

we compute the DTMC describing the transition probabilities

for this time interval. The matrix is shown in the first figure

below in the green cells of columns E through J. This is the

1-step transition matrix. Although all cells of the matrix

below are nonzero, the accuracy of the display shows most as

zero. A discretized cost analysis is shown in cells L through

N.

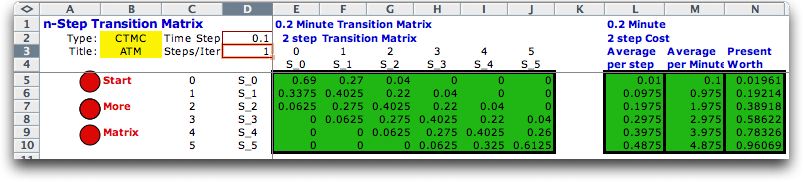

The 2-step

transition matrix is the square of the 1-step matrix. Clicking

the More button

advances the step number to 2 and computes the 2-step

transition matrix as shown in the second illustration.

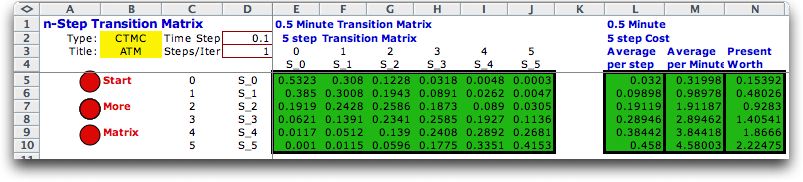

The third case shows the 5-step matrix. With

more and more steps the rows of the matrix will approach the

step-steady-state probabilities. For this example,

five steps are equivalent to only 1/2 minute, so the system

is far from steady state.

|

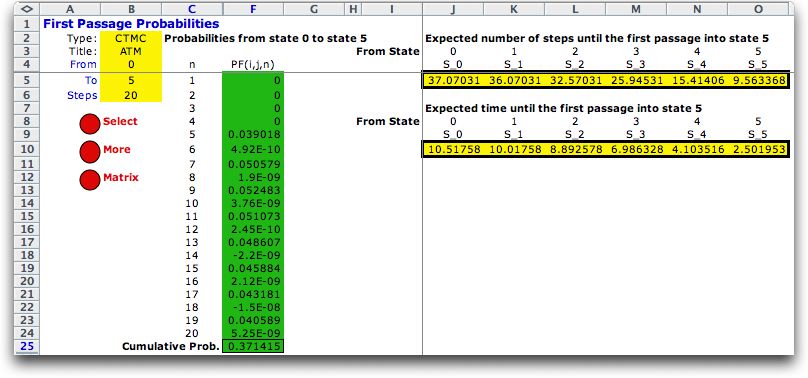

First Pass |

| |

Given some initial state it is

sometimes interesting to compute the probability distribution

for the number of steps required to reach some other

state. The first pass analysis provides this for any two states.

The example below shows the analysis for the number of steps

required to pass from S0 (system empty) to S5 (system

full) for

the first time. The probabilities are shown in the column

labeled PF(i,j,n). The first non-zero entry occurs at step

5. This first passage occurs at step 5 only if 5 consecutive

customers arrive with no departures. Subsequent numbers show

the cyclic nature of the system. The first occurrence of the

S0-S5 transition can only occur with an odd number of events.

The first 20 steps are shown in the table. The sum at the bottom

of column F is the probability that the first transition occurs

in the first 20 steps. We see more steps by clicking the More button.

For recurrent systems the cumulative probability will approach

1.

The analysis also provides the expected number of steps

required to pass for the first time from each state

to the "to" state of the analysis (S5)

in this case. These results start in cell J5. The expected

value for first passage from S0 to S5 is about 37 steps.

The table starting in row J10 shows the expected time of

first passage. The expected first-passage time from S0 to

S5 is about 10.5 minutes. |

|

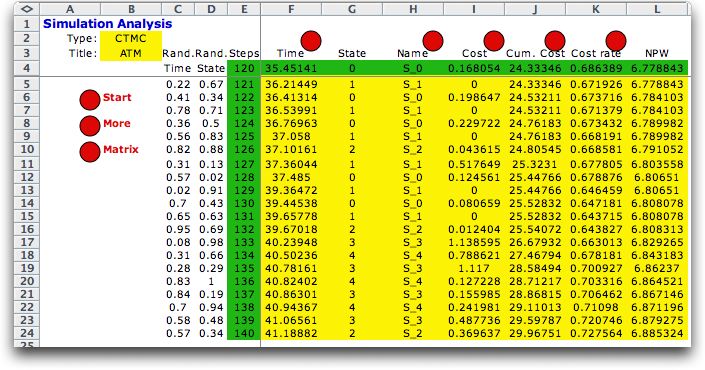

Simulation |

| |

To simulate the CTMC we start

from some initial state and simulate the transitions from one

state to the next. At any given time the system is in some

state and we must simulate both the time and state of the next

transition. In our analysis we simulate both events with Monte-Carlo

simulation and obtain a realization of the random process.

Along the way, we accumulate statistics on time, state and

cost. In the example below we have already simulated 120 steps.

The figure below shows the next 20 steps. The interval shown

is from roughly 35 to 41 minutes. The time column shows the

times of events and the state column shows the resultant states.

The cost column shows the costs associated with the time interval

and transition.

The cumulative cost continues to grow throughout the simulation,

but we expect the cost rate and NPW to approach stead-state

values. |

|

| |

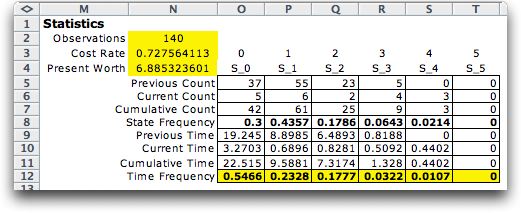

Cumulative statistics from the

simulation are shown in the figure below starting in column J.

The state frequency and time frequency values should approach

comparable steady-state values, however, the example is far from

steady-state. The data shows that the simulated system has never

observed the system full (S5). |

|

Absorbing State Analysis |

| |

Models can be defined with multiple

classes of states, where some states are transient states and

some may be absorbing. Most of the results available for CTMC

are determined by analyzing the embedded DTMC system. |

| |

|

| |

|