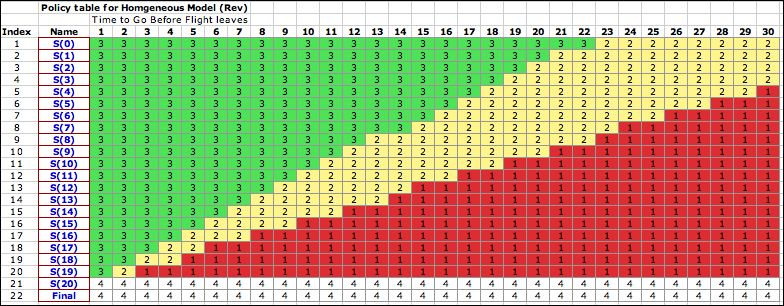

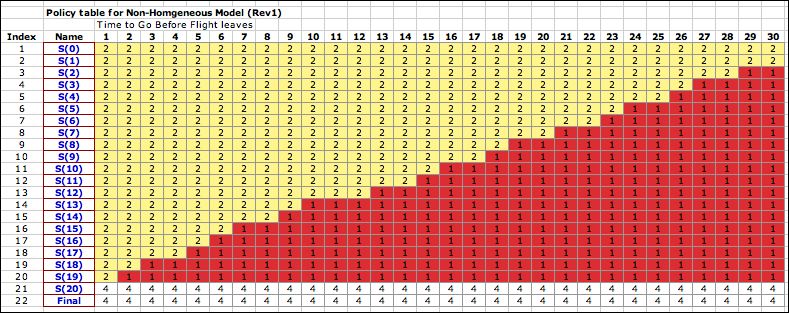

In a more realistic representation,

the model will change over time when different

classes of customers have time-variable arrival rates. Model

Rev1on the example worksheet describes this kind of model. Because

the solver worksheet shows the entire model explicitly, modifications

of the model can be implemented using functions of the step

number. For this case we use the tables below to describe the

variable arrival rates.

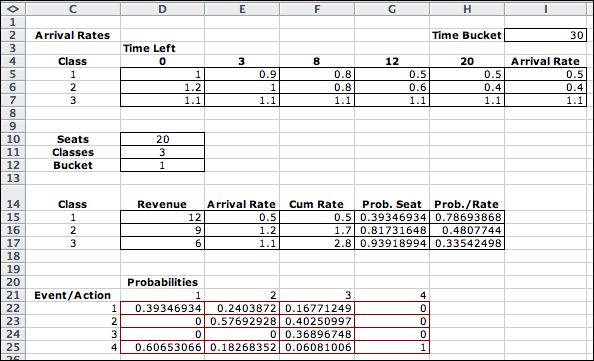

The table at the top shows the arrival rates

by class during five time intervals. The first column (Col.

D, labeled 0) shows the arrival rate for buckets 1 through 2.

The second column shows the arrival rates for buckets 3 through

7, and so on. The current day is in cell I2. This number

is transferred from B12 on the solver worksheet. The current

arrival rates are in cells I5 through I7. They are obtained

from using an Excel Lookup function. The arrival rate is transferred

to the tables below. Ultimately, the bottom table computes

the transition probabilities for each event under each actions.

Action 4 is the null action and event 4 is the null event.

The probabilities are transferred to the transition

probability column on the solver worksheet using the INDEX

function. Now as the iterations progress, the transition probabilities

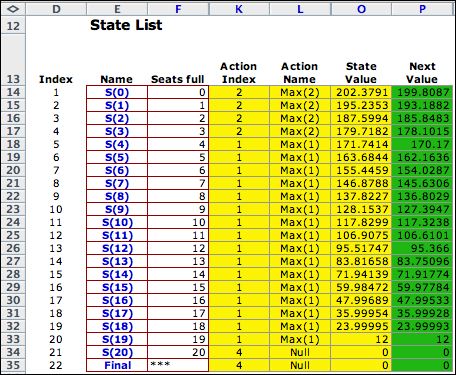

depend on the bucket number. The policy now reflects

the new model. The figure below shows the optimum policy over

the time horizon. It is never optimal to offer the class 3

ticket. |