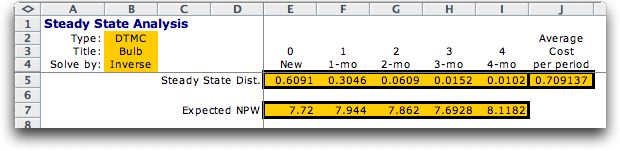

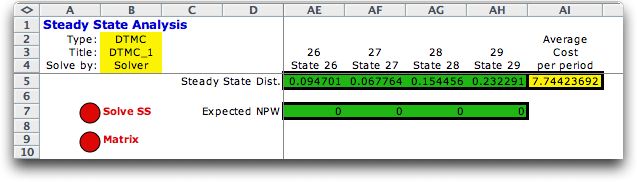

The Steady State worksheet computes

the Markov Chain steady state probabilities. The average

cost per period is computed at the right. The

expected net present worth depends on the initial state

and is computed in the vector below the steady-state

vector.

For the example, we have noted that

the transient solution approaches a steady state, and indeed

this vector is computed independently on this worksheet.

Steady state results are independent of the initial state,

and they are available only for Markov Chains that have

a single recurrent class.