The solution to the problem of

modeling the nonconcave profit functions is to add binary (taking

the values 0 and 1) variables to the model. The

new variables control the order that the pieces of the profit

function are used in the solution. For product Q we need two

new variables and modify the bound constraints for product

Q as below.

From the bounds we see that if  is

0, only is

0, only  is

allowed to be greater than 0. If is

1 and is

allowed to be greater than 0. If is

1 and  is

0, is

forced to 30 and is

0, is

forced to 30 and  is

allowed to increase. If both and are

1, is

forced to 30 and is

forced to 30 and is

allowed to increase. If both and are

1, is

forced to 30 and is

forced to 30 and  is

allowed to increase. is

allowed to increase.

The variables representing R are controlled

by a single binary variable. The variable and revised bounds

are shown below.

Only one variable is necessary because there

is only one convex portion of the profit function. The complete

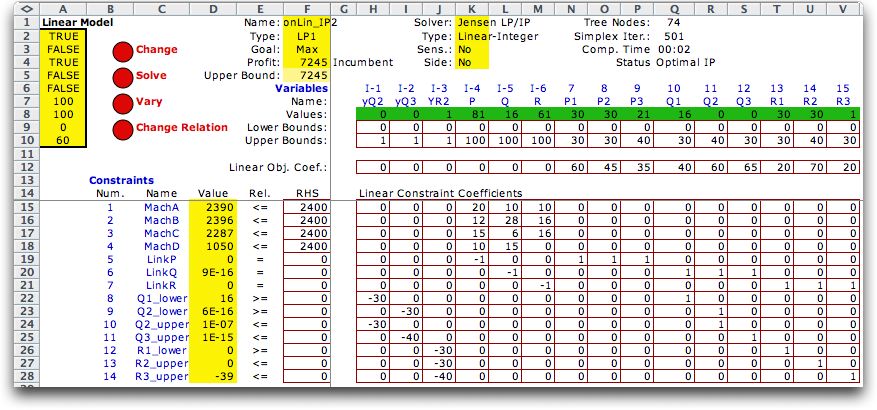

Excel model with the optimum solution is illustrated below. |