|

We illustrate the analysis of the

computer repair problem using screen shots from the Excel add-ins.

The Stochastic

Analysis add-in performs the several different types of analyses

that are illustrated on this page. |

|

| |

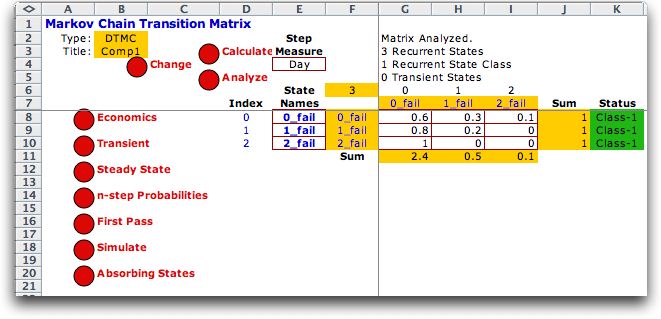

Selecting the Markov Chain

(DTMC) item on the Markov Analysis

menu creates

the DTMC model. Two sheets are constructed, the Matrix worksheet

and the Economics worksheet.

The data from the Model worksheet is automatically transferred

to the two new worksheets. The Matrix worksheet is shown

below. In column G we see an analysis of the current transition

matrix. It has one class of recurrent states. The analysis

cannot determine whether the matrix is cyclic.

Cells are colored to indicate the source of their contents.

Cells outlined in maroon hold user data. Although the data

here was transferred from the Model worksheet it can

be changed by the user. Cells colored yellow hold formulas

created by the add-in. They should not be changed. Cells colored

green are filled by the computer.

The Change button allows the user to change the dimensions

of the matrix. The Calculate button calculates all formulas

in the event the Manual calculation option has been

chosen for the worksheet. The Analyze button performs

the state-class analysis. If the transition probabilities in

the matrix are changed the state-class analysis must be performed

before other analyses can take place.

Buttons arrayed along the left margin perform the analyses

indicated. In each case, clicking a button creates a new worksheet

of the type required by the analysis.

|

|

Economics |

| |

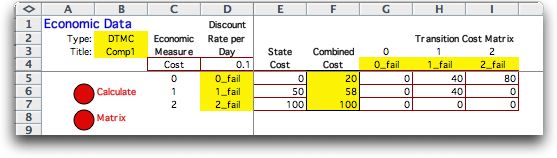

The cost data is entered on the Economics worksheet.

There are two kinds of costs. The state cost is incurred while

the process is in a state, and the transition cost is incurred

when the process moves from one state to another. The discount

rate is for time value of money computations. |

| |

|

Transient Analysis |

| |

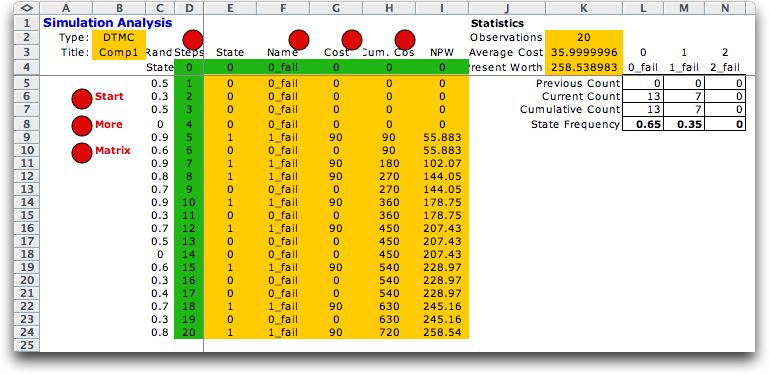

The transient analysis computes

the probability distribution of the state starting from a specified

initial state. In the example below the system starts with

0 failures on the first day. After one day the state probabilities

are as shown in the row labeled 1. The display shows the probabilities

for 20 days or steps. For this example, the probability vector

approaches the steady-state values after only a few days of

the process. Clicking the More button gives 20 additional

days. The Start button allows a different selection

of the initial state.

The program shows the expected values of the step cost, cumulative

cost and discounted cost for each step. |

| |

|

| |

The Chart button creates are

graph of the transient probabilities. |

| |

|

Steady-State Analysis |

| |

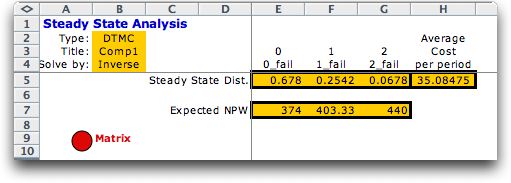

For DTMC's with only a single

class of recurrent states, a steady-state probability vector

can be computed. For acyclic systems, the transient probabilities

converge to the steady-state probabilities as the number of

periods grows. The steady state probability for state j is

the limiting probability that the process is in state j after

a large number of steps. It also equals the long-run proportion

of time that the process will be in state j.

The analysis also provides the expected value (average) or

the per-period cost at steady-state.

|

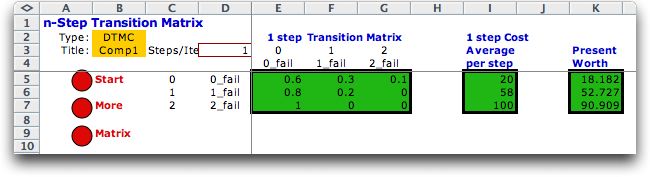

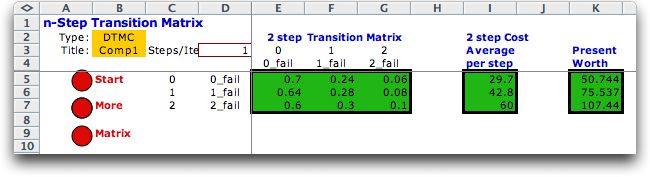

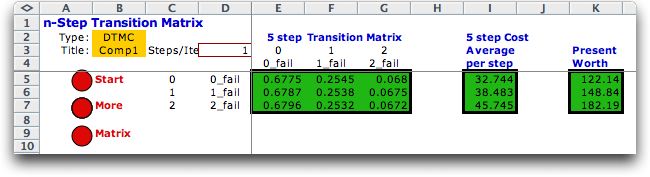

n-Step Probabilities |

| |

This analysis computes a matrix showing

the probability of going from state i to state j in n steps

for all pairs of states. The 1-step probability matrix is just

the transition matrix as shown below. By clicking the More button

the step number is advanced to 2 and the matrix holds the 2-step

probabilities as shown in the second illustration. The third

case shows the 5-step matrix. The rows of the matrix have become

very similar and are all approaching the steady-state vector.

Average step costs and present worth values are also shown.

|

First Pass |

| |

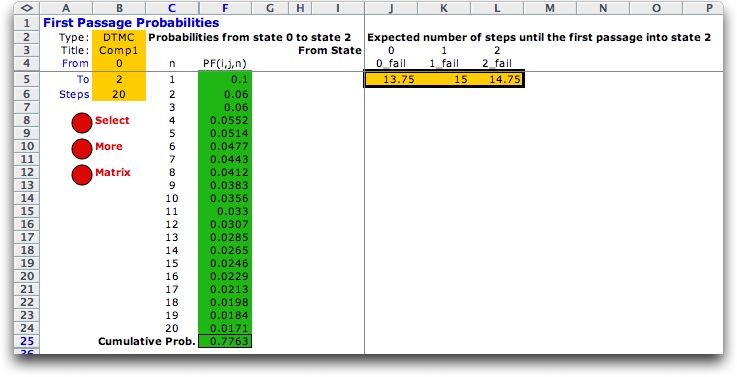

Given some initial state it is

sometimes interesting to compute the probability distribution

for the number of steps (days) required to reach some other

state. The first pass analysis provides this for any two states.

The example below shows the analysis for the number of days

required to pass from state 0 (no failures) to state 2 (2 failures) for

the first time. The probabilities are shown in the column

labeled PF(i, j, n). Note that this is accomplished in 1 step

with probability 0.1, the probability of both computers failing

during a single day. For n > 1, a complex series

of events must occur for the passage to occur for the first

time. At the bottom of the list we see the sum for the first

20 days (0.776). This is the probability that the first passage

occurs in 20 days or less. Clicking the More button,

provides the probabilities for days 21 through 40. The button

can be pressed repeatedly to get the analysis for any number

of days.

The analysis also provides the expected number of steps required

to pass for the first time from each state to the to state

of the analysis (state 2) in this case. These results start

in cell J5. The expected value for first passage from state

0 to state 2 is 13.75 days. |

|

Simulation |

| |

To get some idea of the dynamic nature

of the DTMC it is instructive to perform a simulation. Starting

in a given initial state (state 0 for the example below), the

program simulates 20 days of operation. Transitions are generated

using Monte-Carlo simulation using probabilities from the transition

matrix. Clicking the More button extends the simulation

to 40 days. Any number of days can be simulated by repeatedly

clicking the More button. Cumulative statistics from the

simulation are shown at the right starting in column J. Buttons

above several of the columns create charts of the simulated results. |

|

Absorbing State Analysis |

| |

An absorbing state is a state

that traps the process. Once the process enters an absorbing

state it never leaves. The example considered at this point

does not have an absorbing state, so we change the situation

in the following manner.

| The office manager is tiring of the unreliability of

the computers. He vows that if the day starts with 0 failed

computers he will sell them with a probability of 0.01.

He will then use old-fashioned adding machines. On the

other hand, if ever both computers are failed at the beginning

of the day, he will replace them with new perfectly reliable

computers with a 0.01 probability. Then he will never be

bothered by failures again. |

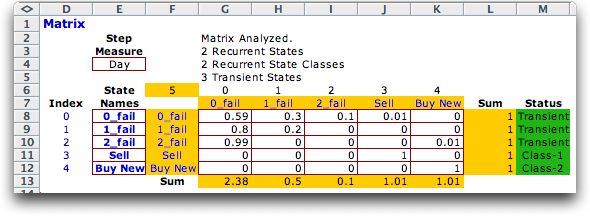

To model this situation we introduce two new states, Sell and Buy

New. The number of states is easily changed by clicking

the Change button on the worksheet and entering the

new number of states (5). The new matrix adjusted for the

situation is shown below. The two states are absorbing states

as indicated with the transition probabilities of 1 on the

diagonal of the matrix. The matrix analysis shows that the

two new states are recurrent states. Once entered, the process

never leaves these two states. The original states are transient

states in that there is a nonzero probability that once the

process leaves one of these states that it will never return. |

| |

|

| |

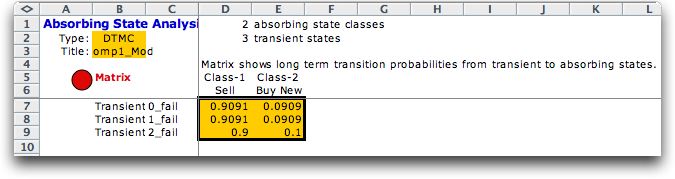

Eventually the system will enter

one of the absorbing states. The question is which will it

enter? This answer can only be given by probabilities because

the transitions that occur are random. The answer also depends

on the state in which the process begins.

The absorbing state analysis on the worksheet shown below

provides useful information. It is apparent that whatever the

initial state there is about a 0.9 probability that the office

manager will eventually sell the computers and only a 0.1 chance

that he will buy perfect ones. If the system begins with two

failures the chance of buying perfect computers is slightly

higher. |

| |

|

| |

|