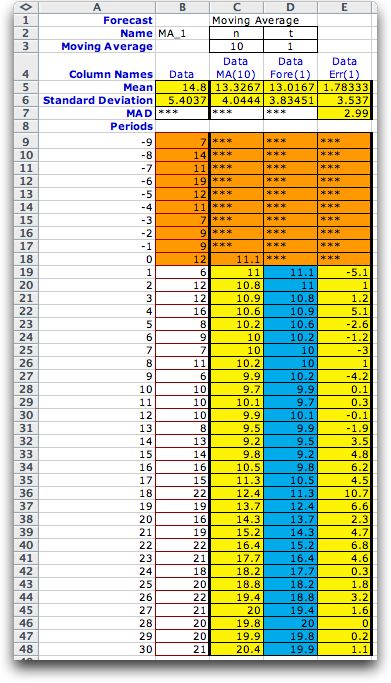

The estimates of the model parameter,

,

for three different values of m are shown together

with the mean of the time series in the figure below. The figure

shows the moving average estimate of the mean at each time and

not the forecast. The forecasts would shift the moving average

curves to the right by ,

for three different values of m are shown together

with the mean of the time series in the figure below. The figure

shows the moving average estimate of the mean at each time and

not the forecast. The forecasts would shift the moving average

curves to the right by  periods.

periods.

One conclusion is immediately apparent from the

figure. For all three estimates the moving average lags behind

the linear trend, with the lag increasing with m. The

lag is the distance between the model and the estimate in the

time dimension. Because of the lag, the moving average underestimates

the observations as the mean is increasing. The bias of the

estimator is the difference at a specific time in the mean value

of the model and the mean value predicted by the moving average.

The bias when the mean is increasing is negative. For a decreasing

mean, the bias is positive. The lag in time and the bias introduced

in the estimate are functions of m. The larger the

value of m, the larger the magnitude of lag and bias.

For a continuously increasing series with trend

a, the values of lag and bias of the estimator of

the mean is given in the equations below.

The example curves do not match these equations

because the example model is not continuously increasing, rather

it starts as a constant, changes to a trend and then becomes

constant again. Also the example curves are affected by the

noise.

The moving average forecast of

periods into the future is represented by shifting the curves

to the right. The lag and bias increase proportionally. The

equations below indicate the lag and bias of a forecast

periods into the future when compared to the model parameters.

Again, these formulas are for a time series with a constant

linear trend.

We should not be surprised at this result. The

moving average estimator is based on the assumption of a constant

mean, and the example has a linear trend in the mean during

a portion of the study period. Since real time series will rarely

exactly obey the assumptions of any model, we should be prepared

for such results.

We can also conclude from the figure that the

variability of the noise has the largest effect for smaller

m. The estimate is much more volatile for the moving

average of 5 than the moving average of 20. We have the conflicting

desires to increase m to reduce the effect of variability

due to the noise, and to decrease m to make the forecast

more responsive to changes in mean.

The error is the difference between the actual

data and the forecasted value. If the time series is truly a

constant value the expected value of the error is zero and the

variance of the error is comprised of a term that is a function

of  and a second term that is the variance of the noise,

and a second term that is the variance of the noise,  . .

The first term is the variance of the mean estimated with a

sample of m observations, assuming the data comes from

a population with a constant mean. This term is minimized by

making m as large as possible. A large m makes

the forecast unresponsive to a change in the underlying time

series. To make the forecast responsive to changes, we want

m as small as possible (1), but this increases the

error variance. Practical forecasting requires an intermediate

value. |