|

|

|

Forecasting |

|

-

Functions |

|

|

|

Many of the

computations for the Forecasting Add-in are accomplished by functions

provided by the add-in. The functions are automatically inserted

into the forecasting forms. They can also be used independently

in worksheet formulas. They are

found in the Excel function list under the heading User Defined

Functions. The function names all have the FF_ prefix. They

are listed below with their arguments. Some of the functions have

range arguments. We show images of forecasts of the various kinds

to discuss the functions and their purposes. In some cases

the activities of the functions could have been carried out with

normal Excel functions or calculations. We use functions so that

missing or non-numeric data will return the text string ***. This

allows the forecasting to continue even when some data is missing.

It is important to remember that user

defined functions are linked to the add-in that created them.

For example, all the function references in the Forecast demonstration

workbook are linked to the add-in in the computer where they

were created. When opened on another computer the reference

includes a path to that add-in. Since obviously the user cannot

open that author's add-in, the reference must be adjusted to

link to the copy of the Forecast add-in on the user's hard drive.

We provide the Relink command on the Forecast menu to fix some

of the references. In particular, any worksheet formula that

uses the function as the first entry after the "="

sign will be corrected. Every function used by the add-in is

placed first in the formula, so all of these references are

corrected by the Relink command.

If the user places a function within

a cell formula, the reference will not be corrected. All such

links can be redirected by the more general Excel Links

command on the Excel Edit menu. |

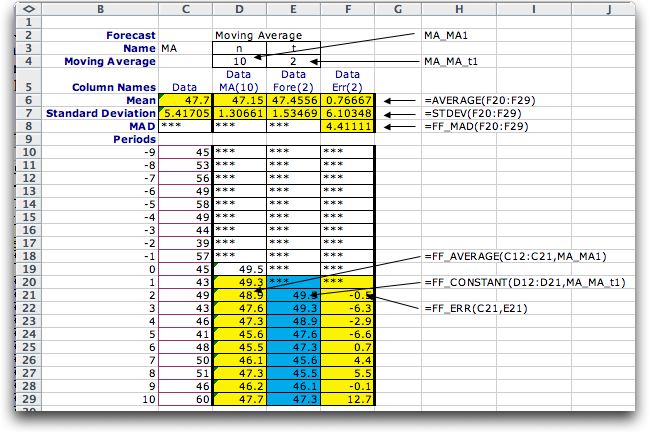

Functions used by Moving Averages |

| |

The functions refer

to two named cells at the top of the display. The length of

the moving average is stored in cell D4 with the name MA_MA1.

The forecast interval is stored in cell E4 with the name MA_MA_t1.

The prefix to the names is the name of the forecast. The figure

below shows the function references used on the worksheet.

The functions are described under the figure.

|

| |

| AVERAGE(F20:F29)STDEV(F20:F29) |

This Excel function is placed in row 6

for each display column. It computes the mean of the entries

in the columns below. Note that the range for the mean

values does not include the warm-up period whose length

is the history. The history value is 10 for the

example. |

| STDEV(F20:F29) |

| This Excel function is placed in row 7 for

each display column. It computes the standard deviation of

the entries in the columns. Again only the data values starting

at observation 1 are considered. At least two numeric values

must appear in the column for a numeric result. |

| FF_MAD(F20:F29) |

| This function computes the mean absolute deviation

of the numbers in a range. The absolute value of each number

in the range is computed and the average of these values

is returned as the result. This is an interesting measure

for forecasting errors because it is increased by the absolute

value of both the mean and variation about the mean of the

errors. The FF_MAD function is only used for error columns. |

| FF_Average(C12:C21,MA_MA1) |

This function computes the moving average.

It has two arguments: a range and the number of values

to be used for the moving average, or the moving average

interval. The number of elements in the range must be at

least as great than the number in the moving average. For

the example, the range has 10 elements and the number in

the average is also 10, so the example computes the average

of the 10 numbers in the range (C12:C21). The function

is useful because it allows experimentation over different

values of the moving average interval. Only numeric values

in the range are used in the average with blanks or strings

contributing to neither the numerator or denominator of

the average. At least one cell in the averaged range must

contain a number. Otherwise the function returns "***".

The example shows the function in row 21. The function

is repeated in rows 20 through 29 with adjusted range references.

This is also true for the other functions described below. |

| FF_CONSTANT(D12:D21,MA_MA_t1) |

This function creates a forecast from a

model that assumes that the time series varies about a

constant mean. It's range covers the moving averages for

10 periods. The second argument indicates the time interval

for the forecast. The value for the interval for the example

is 2 indicating that the forecast is the moving average

value computed two periods earlier. Thus the result for

the example in cell E21 come from the moving average computed

in cell D19. The value of the time interval may be changed. |

| FF_ERR(C21,E21) |

| This function computes the difference between

an observation and a forecast. For the example it computes

the difference between the entry in C21 and the entry in

E21. |

|

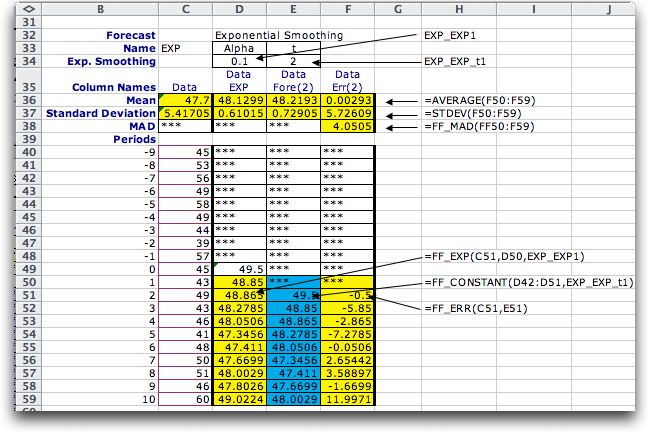

Functions used by Exponential Smoothing |

| |

The figure below shows

the function references used on the worksheet for exponential

smoothing. The functions refer to two named cells at the top

of the display. The value of the Alpha parameter is

stored in cell D34 with the name EXP_EXP1. The forecast interval

is stored in cell E34 with the name EXP_EXP_t1. The prefix to

the name in each case is the name of the forecast. Only the FF_EXP

function is different than those used for the moving average.

It is described under the figure.

|

| |

| FF_EXP(C51,D50,EXP_EXP1) |

This function computes the exponential

smoothing estimate of the time series mean value. It has

three arguments, the current data, the previous estimate

and the value of alpha. For the example in cell D51 these

values appear in cells C51, D50 and EXP_EXP1. |

|

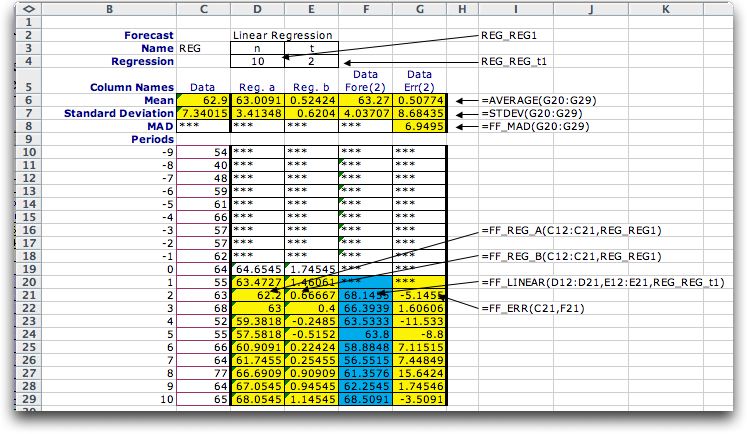

Functions used by Regression |

| |

The figure below shows

the function references used on the worksheet for regression

forecasting. The functions refer to two named cells at the

top of the display. The value of the number of points to be

used in the regression is stored in cell D4 with the name REG_REG1.

The forecast interval is stored in cell E4 with the name REG_REG_t1.

The prefix to the name in each case is the name of the forecast.

The example is simulated from a model with an initial trend

of 1.

|

| |

| FF_REG_A(C12:C21,REG_REG1) |

This function is

used to compute the constant value of a linear regression

equation. The range argument contains the dependent values

used to fit the regression line. Only a specified number

of elements in the range are used. This regression interval

is given as the second argument. For the example, the

range has 10 elements and the number in the regression

is also 10. The independent values for the equation are

the time indices immediately preceding the cell in which

the value is computed. The example computes the

regression constant at time 2. The variable regression

interval is useful for forecasting because it

allows experimentation over different values. The function

is used for regression forecasting. Only numeric values

in the range are used with blanks or strings not contributing

to the result. At least two cells in the range must contain

a number. Otherwise the function returns "***". |

| FF_REG_B(C12:C21,REG_REG1) |

This function is

used to compute the trend value of a linear regression

equation. The arguments are the same as used for computing

the constant term. |

| FF_LINEAR(D12:D21,E12:E21,REG_REG_t1) |

This function is used to make

forecasts with linear models. The first two arguments are

the ranges of the constant and trend estimates respectively.

The third argument is the time interval for the forecast.

The function retrieves the values of A and B computed t periods

earlier and computes.

A + Bt

The example in cell F21 uses the constant and trend values

computed in D19 and E19 respectively. The function returns

"***" if any of its arguments are not numeric. |

|

| |

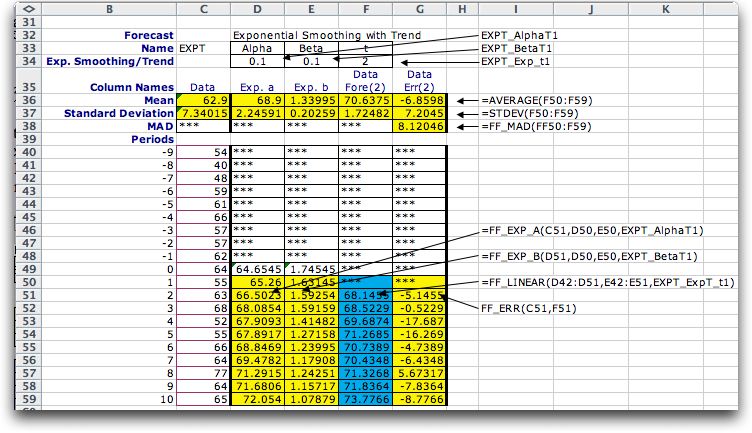

Functions used by Exponential Smoothing with Trend |

| |

The figure below shows

the function references used on the worksheet for exponential

smoothing with a trend forecasting. Another name for this is

double exponential smoothing. The value of the Alpha parameter

is stored in cell D34 with the name EXPT_AphaT1. The value

of the Beta parameter is stored in cell E34 with the

name EXPT_BetaT1. The forecast interval is stored in cell F34

with the name EXPT_Exp_t1. The prefix to the name in each case

is the name of the forecast. The functions unique to this method

are described below the figure.

|

| |

| FF_EXP_A(C51,D50,E50,EXPT_AlphaT1) |

To compute the current estimate of the

mean of the time series this method uses the current observation,

the previous constant estimate, the previous trend estimate

and the parameter alpha. These are the four arguments

of the function. The value returned is the constant value

of the linear equation that will provide the forecast.

If the data argument is missing,

the function provides an estimate based on the other

parameters. When other arguments are missing

or not numeric, the function returns "***". |

| FF_EXP_B(D51,D50,E50,EXPT_BetaT1) |

This function is

used to compute the trend value of the linear equation

based on the current and previous estimates of the constant

term, the previous estimate of the trend and the parameter beta.

These are the arguments of the function. |

|

| |

Functions used by Simulation |

| |

Several functions

are used for simulating a time series as illustrated in the

figure below. The simulation parameters are placed in a parameter

range shown in B8 through B15. Changing numbers in this range

changes the simulated results.

|

| |

| FF_RAND(seed) |

This function returns a random

number drawn from a uniform distribution with range 0

to 1. The function uses the internal Excel random number

generator. The value of the function depends on the seed.

We use this function in the forecast simulations by having

the random number for one period be the seed for the

next. Then by specifying the first seed, the complete

sequence of random values is determined. This is handy

so the same sequence of random numbers can be used in

different simulation experiments. The example is illustrated

in cells B4 through B6. The seed value in B3 controls

the three random values that appear below it. Each call

of FF_RAND uses the previous value as its seed. |

| FF_SimErr(prob, parameter

range) |

This function is used to simulate

the noise of a simulated time series. The function assumes

that the noise is Normally distributed with 0 mean. The

standard deviation of the noise is the third cell in

the simulation parameter range. For the example, this

is in cell B10. The Monte Carlo method provides the simulated

value. The prob argument is a uniformly distributed

random variable provided by the FF_RAND function. The

example in cell E8 computes the simulated value from

the random number in B4. |

| FF_SimChange(probchg,

probvalue, parameter range) |

This function computes either trend changes or step

changes in the simulated series. For both, there is a specified

probability that a change will occur (0.1) for the example

below. If it does occur there is a specified mean (0) and

standard deviation (1) of the amount of the change. Two

random numbers are required to evaluate the function. The

argument probchg is the random number determining

if a change does occur. If this random number is less than

the probability of change, the change occurs.

If the change occurs, the second random number, probvalue,

is relevant. It then determines the magnitude of the

change. The probability of change, the mean value of

the change and the standard deviation of the change are

provided by the parameter range. For the example in cell

E12, the random number in B5 is more than the change

probability, so no change is experienced. Thus, we see

the value of 0 in E12. |

|

| |

Other Functions |

| |

Two other functions are

used in forecasts that involve seasonality and portfolios. |

| |

| FF_ADJUST(factor1, factor2) |

This function simply

multiplies factor1 by factor2. It is used in for forecasts

involving seasonality. We use this function rather than

simply multiplying the two numbers together because the

function returns the text string *** when one of its

arguments is not numeric rather than an error indication. |

| FF_SUMPRODUCT(range

1, range 2, interval 1, interval 2, start 1, start 2) |

This function is does the same

as the Excel SUMPRODUCT function except on different

size ranges. Elements of the two ranges are in range

1 and range 2. The numbers in range 1 to

be summed are in columns that differ by interval

1. The numbers in range 2 which are to be multiplied

by the numbers in range 1 are in columns that differ

by interval 2. The arguments start 1 and start

2 indicate which elements are to be summed. Examples

are below when range 1 = (1, 2, 3, 4,

5, 6) and range 2 = (1, 2, 3, 4)

FF_SUMPRODUCT((1, 2, 3,

4, 5, 6),(1, 2, 3, 4),3, 2, 1, 1) = 1*1 + 4*3 = 14

FF_SUMPRODUCT((1, 2, 3, 4,

5, 6),(1, 2, 3, 4),3, 2, 2, 2) =2*2 + 5*4 = 24

FF_SUMPRODUCT((1, 2, 3, 4,

5, 6),(1, 2, 3, 4),3, 2, 3, 1) = 3*1 + 6*3 = 21

The function is used in Portfolio forecasts. |

|

| |

|

|