The example on this page is from

the field of stochastic programming. Some

of the

parameters

of

a

situation

are originally not known with certainty, however, probability

distributions for their values are given. Certain decisions

must be made before the random variables are realized. After

they are realized, other decisions may be made. The latter

are called the recourse decisions, and this type of

problem is called decision making with recourse. We

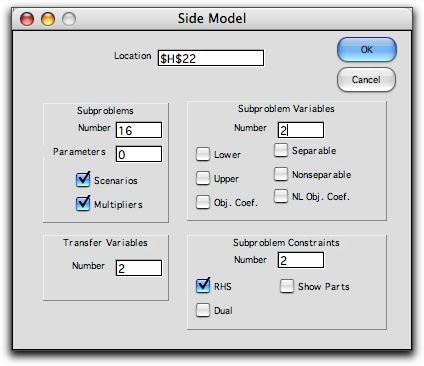

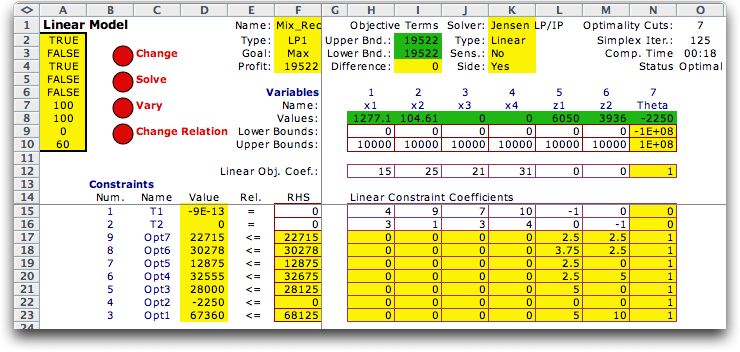

use the Jensen LP/IP add-in to solve the example, thus providing

an illustration of the L-shaped method.

This example was borrowed from An Optimization Primer,

An Introduction to Linear, Nonlinear, Large Scale, Stochastic

Programming and Variational Analysis, by Roger J-B Wets,

January 11, 2005 (unpublished manuscript). A separate section

of this site considers Stochastic

Programming in detail.

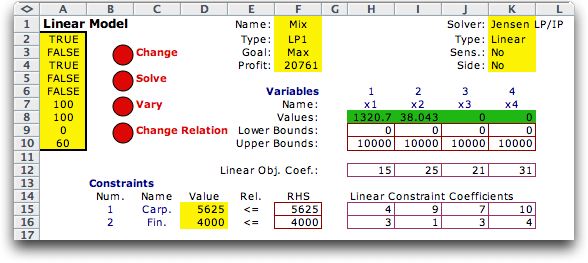

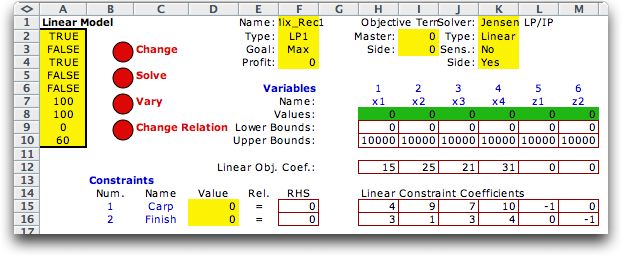

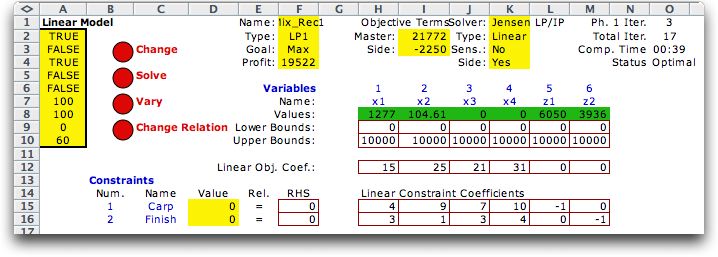

Consider a product

mix problem. A furniture maker

makes

four

products:

P1, P2,

P3 and P4. Two manufacturing resources are required: carpentry

and finishing. The requirements

measured in hours per unit are known and shown in the table

below along with the profit per unit of product.

Product Parameters |

P1 |

P2 |

P3 |

P4 |

Carpentry Hours per Unit |

4 |

9 |

7 |

10 |

Finishing Hours per Unit |

3 |

1 |

3 |

4 |

Profit per Unit |

15 |

25 |

21 |

31 |

Our problem is to select the product mix to maximize total

profit, but the availability of the resources are not known.

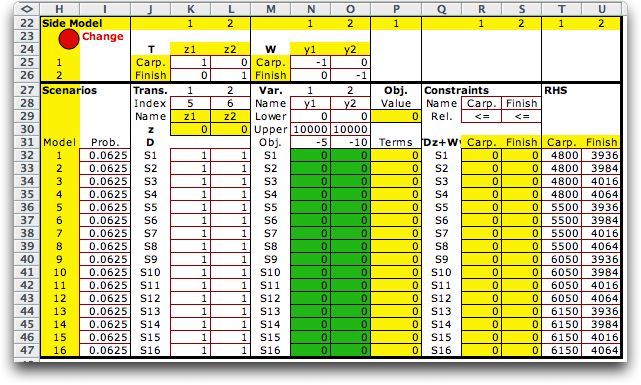

Rather we have four equally likely estimates of the hours

available for each resource.

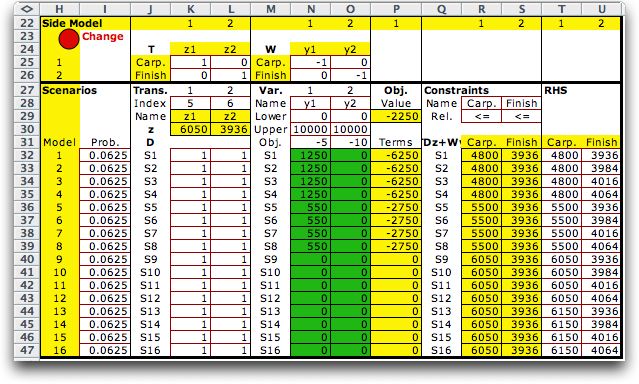

Resource Distribution |

1 |

2 |

3 |

4 |

Carpentry Hours Available |

4800 |

5500 |

6050 |

6150 |

Finishing Hours Available |

3936 |

3984 |

4016 |

4064 |

Probability |

0.25 |

0.25 |

0.25 |

0.25 |

The mix chosen will require some number of hours for the resources.

Depending on the amount that is available we will pay for extra

hours to obtain the necessary number of hours.

This is called a decision making with recourse. We must chose

the mix before the uncertain quantities are known. Once the

uncertainty is realized we must make additional decisions,

called the recourse decisions, to adjust for the new conditions.

We use the notation below to describe the model with accuracy.

For the example the possible values of the random variables

are given in the table above. The probabilities associated

with these values are 0.25.

|