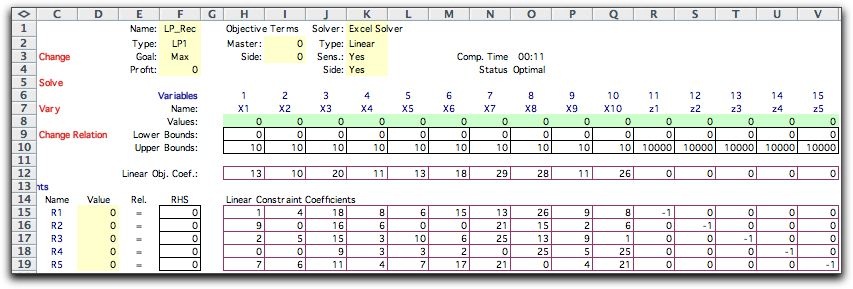

When the distribution of a random variable is continuous rather

than discrete, we will approximate the distribution with either

a discrete distribution or a piece-wise uniform distribution.

In this section we deal with the discrete approximation. We

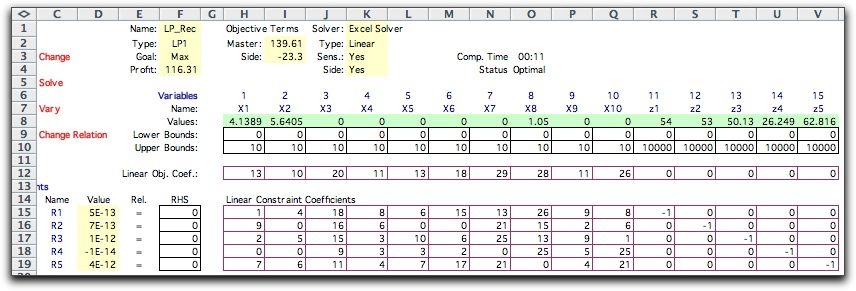

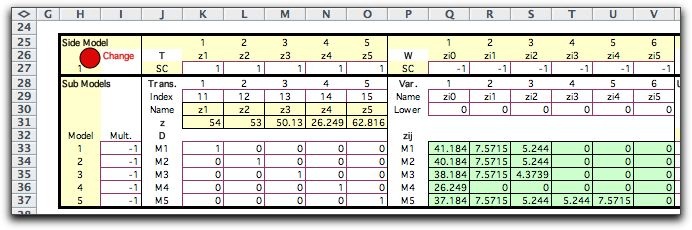

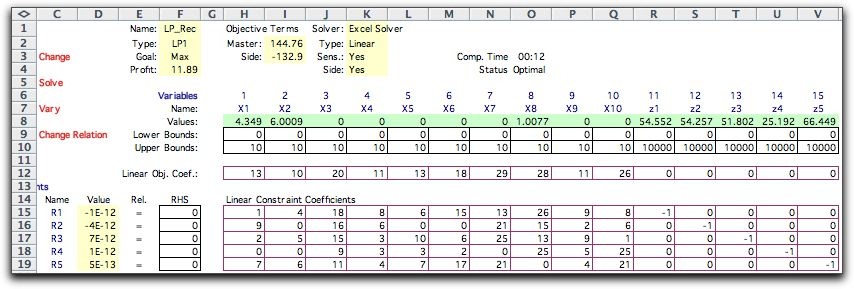

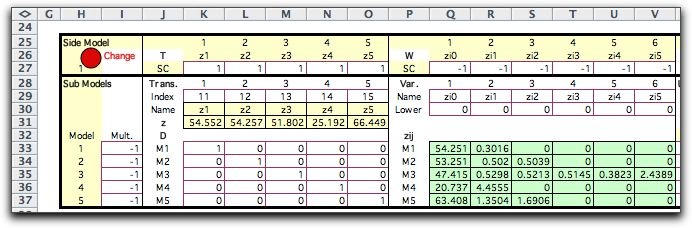

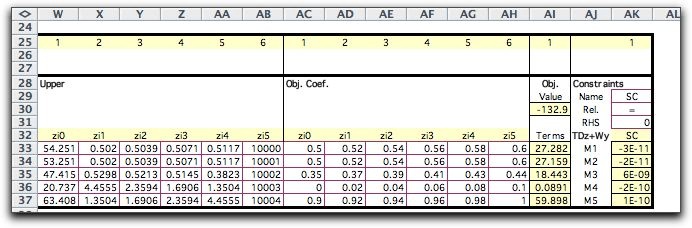

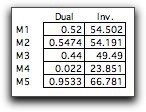

will illustrate this application with a simple-recourse model

of the LP situation used at the beginning of this section.

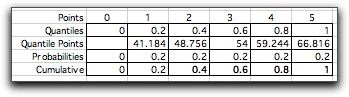

To approximate the continuous distribution we select K+1

quantile values ranging from 0 to 1.

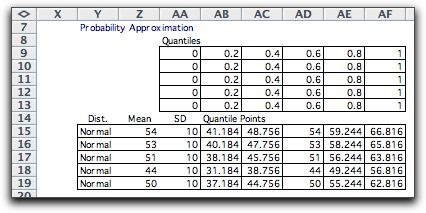

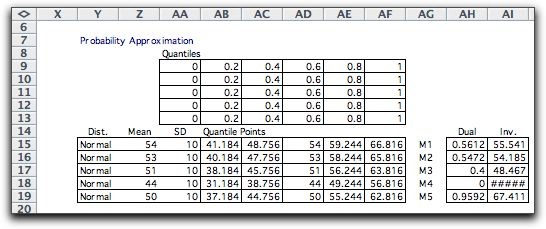

To illustrate, consider a Normal distribution

with mean 54 and standard deviation 10. We divide the probability

range into five intervals using the quantiles: 0, 0.2,

0.4, 0.6, 0.8, 1. The quantile points are computed with the

RV_Inverse function of the Random Variables add-in.

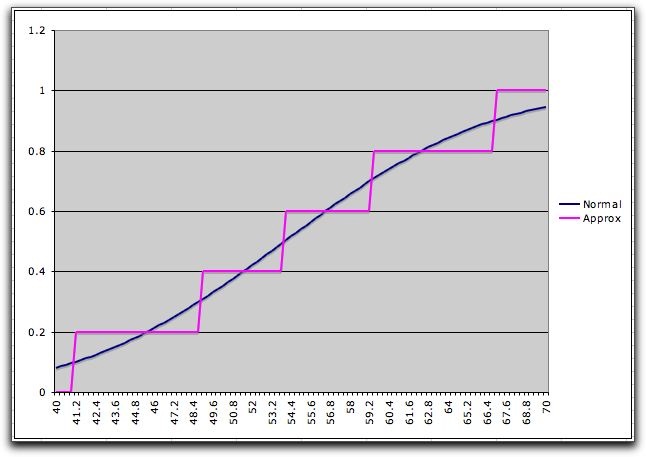

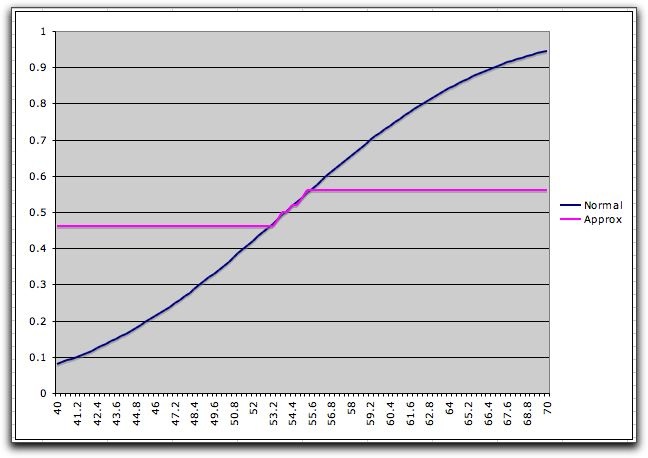

The graph below shows the cumulative distribution

of this discrete approximation along with the Normal distribution.

The construction of the graph shows the steps as ramps, but

the steps are immediate at the quantile points. The approximation

sometimes over

estimates

the

continuous cumulative and sometimes underestimates it.

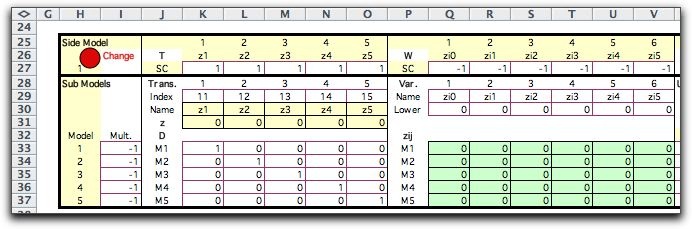

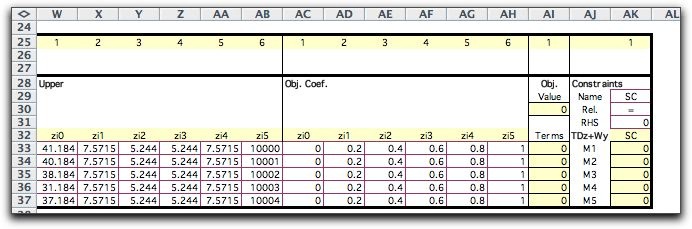

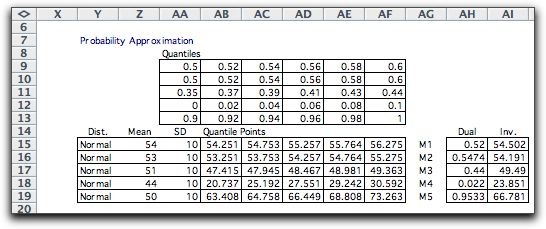

The number of steps and the selection of the

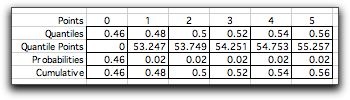

quantiles controls the accuracy of the approximation. The table

below shows a selection of quantiles that emphasizes the range

0.46 through 0.56.

The cumulative distribution is more accurately

represented in this range, while it is not well approximated

outside the range. This feature will have usefulness for the

simple recourse model.

|