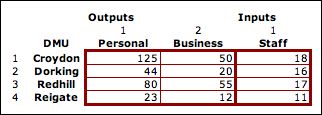

One way to compare

the branches is to add together the two output measures to

obtain a single measure. The table below shows the combined

outputs with the title transactions. The number of

transactions is simply the sum of the personal

and business transactions shown in the data table.

With only one output and one input we can compare DMU's by

computing the ratio: output/input or transactions per staff

member. The Ratio column

is obtained by dividing the transactions

number by the staff number. This suggests that Croydon is

the best branch because its ratio is larger than all the rest.

For convenience we want a measure

that lies between 0 and 1, so we divide the ratios by the maximum

ratio (9.72). The results for the four branches are in the

column above labeled Efficiency.

Efficiency is a good word for the measure since it divides output

by input and is similar to comparisons made in other fields.

For instance one can speak of the efficiency of a solar

cell by dividing the electrical power produced in the cell

by the light power falling on the cell. Both

input and output power are measured in watts.

The quantities are difficult to measure, but efficiency compares

the result to a standard to obtain a meaningful value. For

instance the record for solar cell efficiency is 42%.

One would expect that solar cell efficiency will never approach

1.

The efficiency

number computed in the table above is not the same. The

value of 1 does not mean Croydon is perfectly translating inputs to outputs.

It only means that Croydon has the best output over input ratio of the four

banks. If one accepts the measure it can be used to rank the four DMU's. The

result is shown in the rank column. The CFO

has the result that she needs. She brings her ranking to a meeting with the

branch managers.

The manager of the Croydon branch is pleased, but the other

branch managers call the ranking unfair. They say the measure

used to obtain the ranking is flawed. Simply adding the outputs

may not be correct. Different efficiencies would be obtained

if a different weight were applied to each measure. One could

say that the personal transactions were not as important as

the business transactions. Someone could propose that each business

transition be given three times the weight of a personal transaction.

This would yield different efficiency values and perhaps a different

ranking.

The CFO does not want to pursue a policy that alienates

the managers. No one, except the Croydon

bank manager will accept the efficiency as calculated above to compute the

ranking. If the branch managers accept the idea that some ratio of outputs

to inputs can be used for comparison, the problem is to agree on

the best weights for the output factors. Of course, the branch managers

will not agree on the appropriate weights.

The operations analyst attending the meeting suggests to the CFO that the

DEA method might help in seeking agreement. After a private discussion with

the analyst, the CFO announces that the managers may independently weigh the

factors

any way they like. The CFO adds that the managers must each use

the input and output data (from the tables above) and

evaluate the efficiencies for all four branches with the same set of weights.

Each branch must work without interacting with any other branch. The managers

agree to the restrictions and agree to meet in one week to provide

their answers.

DEA is a method to deal with situations like this. Although it does not solve

the ranking problem directly, the DEA provides some objective measures to obtain

a partial ranking. The DEA add-in embodies the computational tools necessary

to implement the method.The following pages of this section describe the method

along with the add-in features. Only the basics of DEA are presented. There

are many papers and books on the subject as reported in a web site by Emrouznejad.

Several commercial programs provide more detailed analysis than this add-in.

There are many practical questions involved with actual implementations that

are not considered here. |