|

When the distribution of a random variable is continuous rather

than discrete, we will approximate the distribution with either

a discrete distribution or a piece-wise uniform distribution.

In this section we deal with the discrete approximation. We

illustrate this application with a simple-recourse model

of the LP situation used at the beginning of this section.

To approximate the continuous distribution we select K+1

quantile values ranging from 0 to 1.

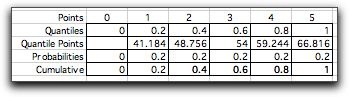

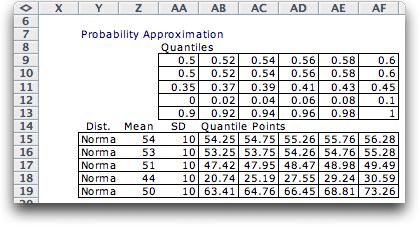

To illustrate, consider a Normal distribution

with mean 54 and standard deviation 10. We divide the probability

range into five intervals using the quantiles: 0, 0.2,

0.4, 0.6, 0.8, 1. The quantile points are computed with the

RV_Inverse function of the Random Variables add-in.

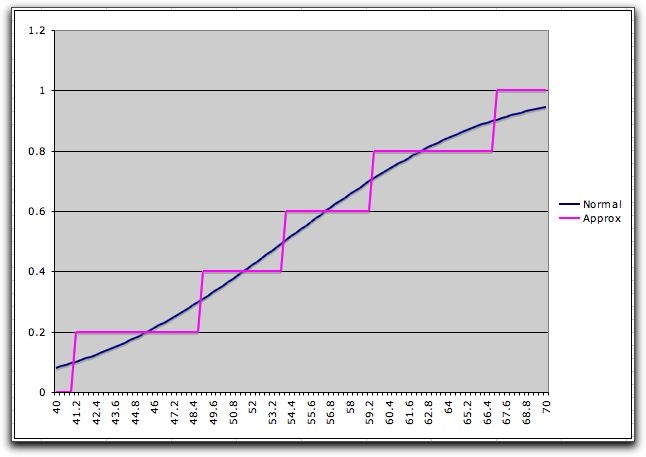

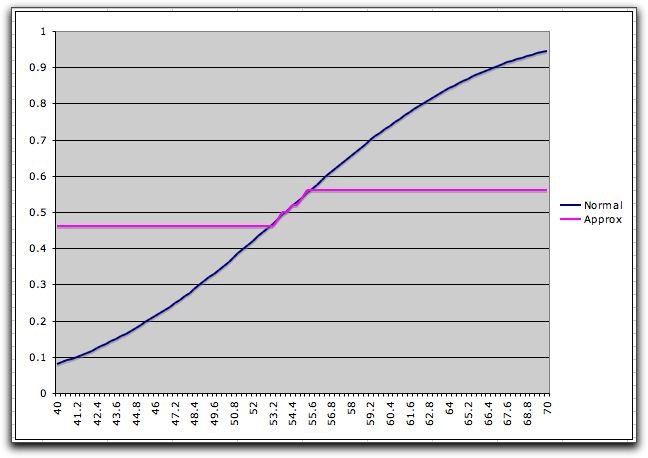

The graph below shows the cumulative distribution

of this discrete approximation (in magenta) along with the

Normal distribution (in blue). The picture shows the steps

as ramps, but the steps are perpendicular at the quantile points.

The approximation sometimes over

estimates

the

continuous cumulative and sometimes underestimates it.

The number of steps and the selection of the

quantiles controls the accuracy of the approximation. |

Simple Recourse |

| |

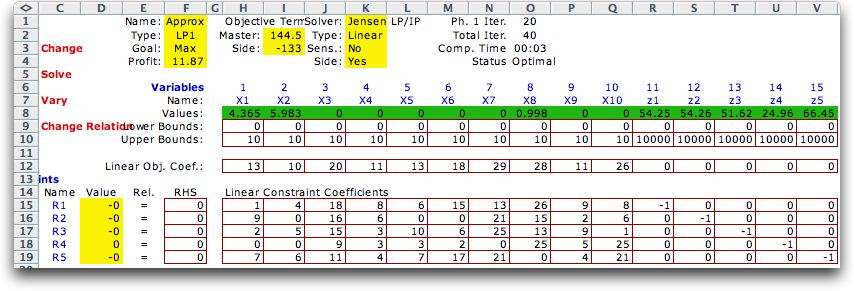

We return to the ten product

mix problem considered earlier, but now we will solve it as

a simple-recourse model. The master problem below includes

the production variables and the variables computing the resource

usage. |

|

| |

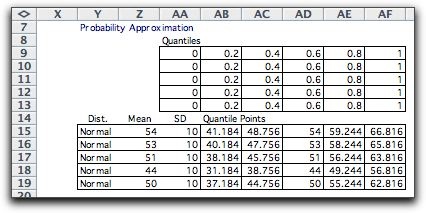

To the right of the model we have constructed

tables to compute the necessary probabilities and quantile

points from the quantile values specified by the modeler. Normal

distributions are defined in columns Y through AA. All computations

relating

to these distributions are provided by functions in the Random

Variables add-in. Other distributions could just have

well been used.

The piecewise linear representation of the expected

recourse costs are expressed in the side model. Build the side

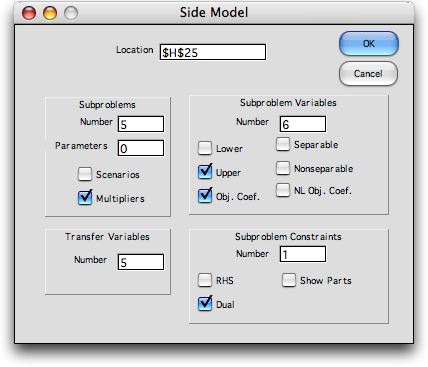

model by choosing Side Model from the Math Programming menu.

Fill in the dialog as below.

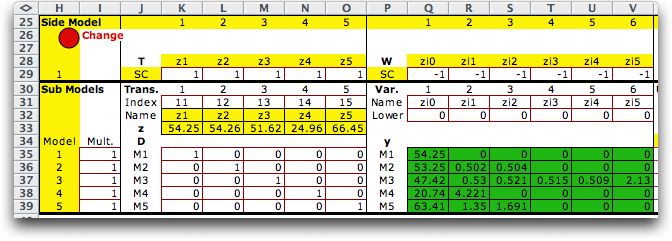

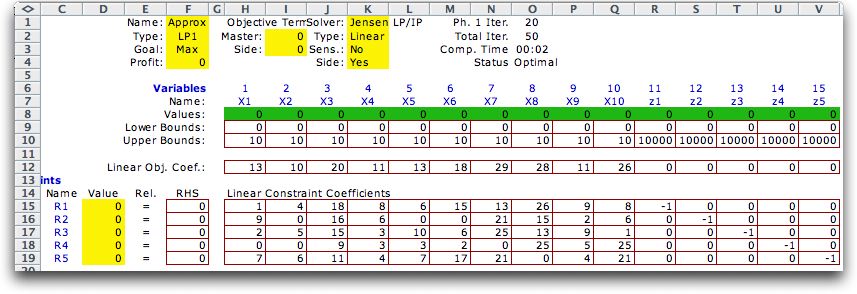

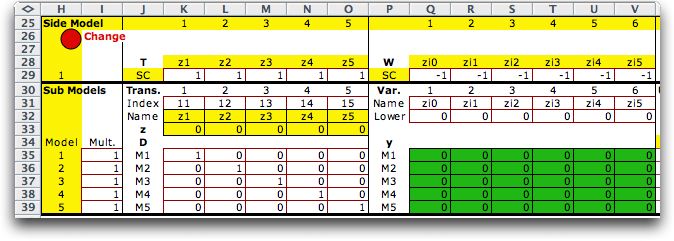

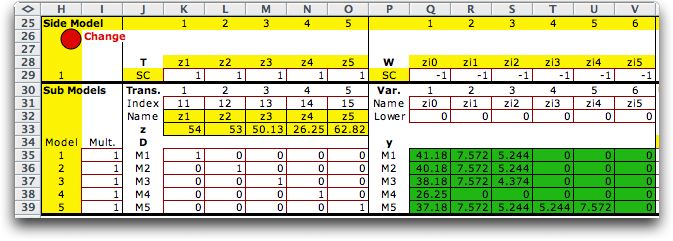

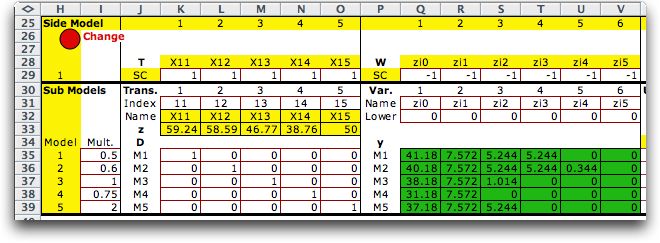

The model is constructed starting in cell H25.

We show the model in two parts below. The first part identifies

the linking variables through the indices in row 30. Columns

J through O provide information on T and D.

The variables and the associated W matrix

are in columns P through V. For definitions of the matrix terms,

see the side

model discussion. The multipliers in column I represent

indicate the penalties associated with the violating the resource

constraints. For this discussion we charge $1 for each unit

of resource shortage and $0 for each unit of resource overage.

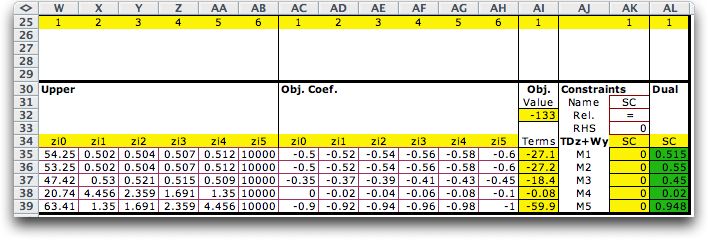

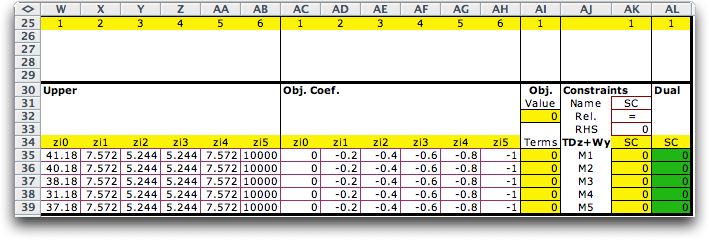

The upper bounds defining

the piecewise approximation are in columns W through AB. The

associated objective coefficients are in AC through AH.

The numbers in these cells are linked by formulas to the table

constructed for the piecewise linear approximation. For details,

see the demonstration workbook for this section.

The constraints

in AK require the equality between the linking variables and

the pieces. The relation and limit of the side constraints are

in cells AK32 and AK33 respectively.

|

Solution |

| |

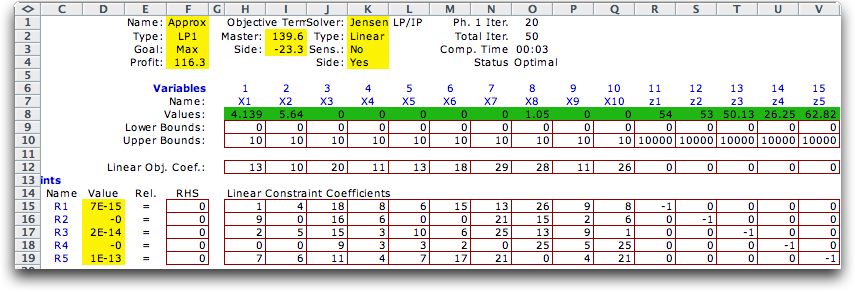

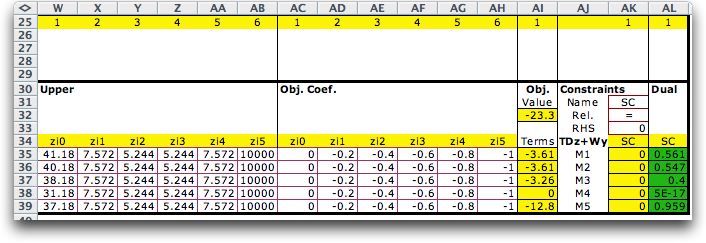

Clicking the Solve button at the top

of the page provides the solution shown below. The resource

usage variables, z1 through z5, are in both the master and

subproblems. The production variables are x1 through x8. The

green cells in the side model show the results for the pieces

of the piecewise linear form. |

|

| |

The important point of this discussion

is that simple recourse is relatively easy to model and solve

with linear programming. The individual stochastic part of

the problem is modeled with a deterministic equivalent. The

expected cost of the resources are piecewise approximations

of the continuous expected cost function.

More accuracy may

be obtained by adding more pieces to the approximation or more

accurately representing the expected value in the region of

the optimum. The search is aided by the dual variables of the

side constraints shown in column AL of the figure above. This

approach is considered below. |

A Better Approximation |

| |

The solution obtained above provides

information about the optimum use of the resources of

the product mix problem. In particular the dual variables shown

in column AL show the probabilities that the resources will

be violated at the optimum solution. The first resource,

represented by the first side constraint, has a dual variable

of 0.561. Solution uses 54 units of R1 and the mean availability

of R1 is 54 so really the risk of violating the resource is

0.5. Our piecewise approximation causes the error of 0.061.

We

obtain a more accurate approximation by defining quantile points

that emphasize the probability range 0.5 through 0.6.

The cumulative distribution shown below is more

accurately represented in this range, while it is not well

approximated outside the range. This feature will have usefulness

for the simple recourse model.

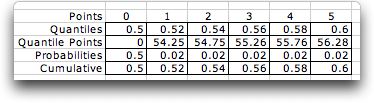

Based on the solution found with the rough

approximations for the Normal distributions, we modify the

quantiles under consideration to cover a smaller range of probabilities.

In

the table below

we define five intervals in a 0.1 range for each random variable.

The optimum solution is shown below for the

revised quantiles. The value of the expected recourse cost

is quite distorted by the approximation,

so the optimum objective function is markedly different for this

solution. The approximation adds a negative constant to all solutions,

so the decision values obtained are the optimum for the more

accurate representation. The slopes of the terms of the objective

function of the LP determine the optimal solution, and the

slopes in the smaller range are much more accurate

than with the first approximation. |

|

| |

The dual solution provides an

interesting interpretation. The dual indicates the risk that

each constraint will be violated when the optimum solution

is pursued. Clearly the last constraint, indicated by M5, is

the most important constraint. The solution will have a shortage

with respect to this RHS in over 95% of the future realizations.

Apparently, the profit obtained by using more of this resource

is sufficient to pay for the cost of its violation. Of course

the optimum solution and the risks depend on the penalties.

The two solutions are compared in the table.

|

Different Penalties |

| |

The multiplier column holds the penalties for

constraint violation. For the example below, we have set different

penalties for each constraint. We are using the simple equal

probability approximation of the resource availability distributions.

Of course the solution depends on the weights. To find the risk

values, you must divide the dual values by the weights. |

|

| |

The methods described on this page can be used

to solve a variety of interesting stochastic programming problems.

Each random RHS adds a collection of variables representing the

parts of a piece-wise linear function. The parameters of the

parts are easily determined by quantiles selected by the user.

The quantiles can be varied to obtain more accurate representations

in the region of the optimum. The random variables add-in

allows a large variety of distributions for the random variables

with little or no changes in the model. |

| |

|