|

To illustrate a recourse problem, we consider a capacity expansion

problem that has the form of a transportation problem. This example

was contributed by David Morton at the University of Texas.

A company will supply electricity to three demanders from

two electric generators. The unit cost of supplying each customer

from each generator site is given below.

Transport Cost |

Dem. 1 |

Dem. 2 |

Dem. 3 |

Gen. 1 |

4.3 |

2 |

0.5 |

Gen. 2 |

7.7 |

3 |

1 |

The amounts required by the three demanders is uncertain.

Each demand has three levels with amounts and probabilities

given below. The probability distributions are independent.

Demand/ Probability |

Dem. 1 |

Dem. 2 |

Dem. 3 |

Level |

|

|

P(  ) |

|

|

|

P(  ) |

|

|

|

P(  ) |

|

|

|

|

|

|

|

2 |

|

|

|

|

3 |

|

|

|

To supply the electricity, the company will install capacity

at the two generators. The first-stage decisions are  and and  ,

the installed capacity at the two generators. The unit costs

of installed capacity are $400 and $350 at generator 1 and

2 respectively. The total capacity cannot exceed 10,000. ,

the installed capacity at the two generators. The unit costs

of installed capacity are $400 and $350 at generator 1 and

2 respectively. The total capacity cannot exceed 10,000.

The reliability of the installed capacity is uncertain. The

fractions  and and  are

the proportions of the installed capacity that will actually

be available for satisfying demand. There are three levels

of reliability as given in the table. These probability distributions

are independent. They are also independent of the demand random

variables. are

the proportions of the installed capacity that will actually

be available for satisfying demand. There are three levels

of reliability as given in the table. These probability distributions

are independent. They are also independent of the demand random

variables.

Reliability/ Probability |

Reliability 1 |

Reliability 2 |

Level |

| |

P( ) |

|

| |

P( ) |

|

|

|

|

|

|

2 |

|

|

|

3 |

|

|

The decision maker must select the generator capacity to install

before knowing the demand or reliability. The second-stage

decisions are the decisions about which demands to service

from the generators. In the following  is

the demand satisfied at customer j from generator i.

We add a third supplier, Subcontract, to represent

demand not met from the generators. The cost can be viewed

as a penalty cost or as the cost of satisfying the demand through

a subcontractor. is

the demand satisfied at customer j from generator i.

We add a third supplier, Subcontract, to represent

demand not met from the generators. The cost can be viewed

as a penalty cost or as the cost of satisfying the demand through

a subcontractor.

The problem has the form of a transportation model as shown

below with random variables and decisions affecting the supplies

and demands.

Transport Cost |

Dem. 1 |

Dem. 2 |

Dem. 3 |

Supply |

Gen. 1 |

4.3 |

2 |

0.5 |

|

Gen. 2 |

7.7 |

3 |

1 |

|

Subcontract |

6000 |

6000 |

6000 |

no limit |

Demand |

|

|

|

|

The transportation model cannot be immediately solved because

its parameters depend on five random variables and two decisions

determined elsewhere. |

The Recourse Model |

| |

To find the optimum

values of the generator capacities, we setup a recourse model. The

first-stage problem is to select capacities for the generators.

First-Stage Model

|

The second-stage problem is to distribute the electricity.

Second-Stage Model

|

The two models can be combined to form a deterministic linear

programming model that represents all 243 combinations of

the

random variables explicitly. This model has 2,189 decision

variables and 1,216 structural constraints. The free Solver

that comes

with Excel is not able to solve a problem of this size, but

it is possible to set the problem up using the Math

Programming

add-in.

The problem may be solved with the L-shaped method available

through the Jensen LP/IP add-in. The master problem describes

the variables for the generator capacity

and the

limit on the

maximum

capacity.

The

second

constraint shown is irrelevant. The arbitrary solution (2000,1000)

is shown for illustration.

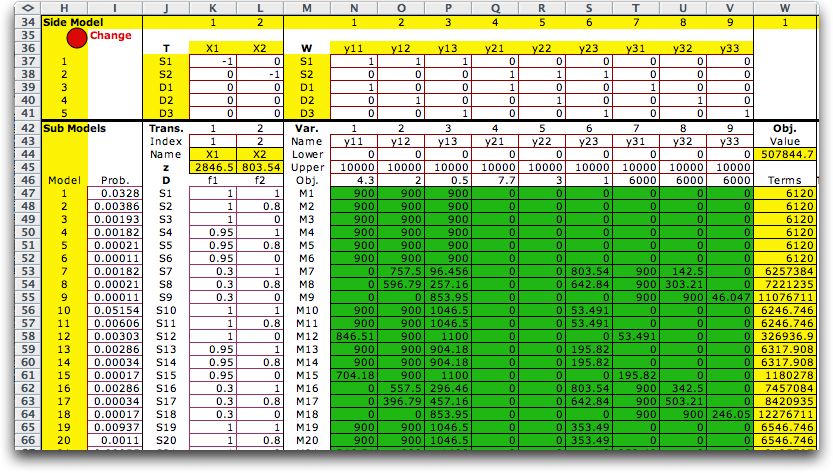

The side model has a row for each scenario. To

reduce the width of this page we show the model in two parts.

Only 20 submodels are shown, but there are 243 in total. The

part of the model representing the transfer variables (generator

capacities)

and subproblem

variables

(distribution

decisions) is shown below. To optimize the subproblems for

the given master problem solution, click the Solve button

near the top of the worksheet and then choose the Solve

Side Problem option

of dialog.

The

optimum solution for the first 20 sub models is shown in the

green cells below. Ths solution depends on the variable values

chosen for the master problem (2000, 1000). |

|

| |

The remainder of the form shows the constraints

of the subproblems. The relations are entered in row 32. The

RHS values are different for each scenario and are prescribed

in columns AD through AH. The yellow fields in columns Y through

AC show the value of each constraint for the current solution.

Comparing the constraint values to the RHS values will show that

all subproblem solutions are feasible. If some subproblem has

no feasible solution, the corresponding solution row has "***"

in the solution cells. When this happens, the remaining sub models

are not computed and the solution is meaningless. |

| |

|

Solving the Problem |

| |

When the Solve button at the left

of the master problem is clicked the problem is solved (assuming

it is feasible and not too large). If the Excel Solver is

used to find the solution, the model of the entire combined

master and subproblems is formulated and solved with the Excel

Solver. For the current example, this option will not work

because the free solver thant comes with Excel can only solve

small problems. More advanced solvers available from Frontline

Systems can

easily solve problems of this size.

When the Jensen LP/IP is the solver of choice, the

dialog below is presented. The first option of

the dialog is to solve the combined master and subproblems with

the simplex method. The LP/IP solver has no built-in limits

on the size of the problem and the add-in will attempt to solve

the problem. The complete problem was solved on the authors

Apple IBook computer running Excel 2007 under the Vista operating

system solved the problem in about three minutes. Using Excel

2003 with the Mac OS 10.4.11 operating system took considerably

longer.

The second option calls a decomposition algorithm called the

L-Shaped Method. These results are demonstrated below. The

third option solves only the Master Problem neglecting the

subproblems. The fourth option solves the side problem for

a given master problem solution.The last two options are considerably

easier than solving the combined problem.

|

L-Shaped Method |

| |

By choosing the decomposition option, the add-in

presents the L-shaped algorithm dialog. This method is described

more fully in the section on Side

Models for the Math

Programming add-in. The dialog below specifies that

the output is to include the cut constraints

along with the final solution.

After 13 optimality cuts and 7345 simplex iterations

requiring 21 seconds on the author's computer we obtain the

solution below. This is not the optimum because a gap of 2.66

remains between the lower and upper bounds. The tolerance is controlled

on the dialog. |

|

| |

The subproblem solutions are shown on the side

models. Only 20 sub models are shown. |

|

| |

The last three recourse variables are introduced

so that every sub model has a feasible solution. Each has a

large objective coefficient (6000) that penalize solutions

that have nonzero values for one or more of these variables.

They represent infeasibility conditions with regard to the

original problem statement. We see for example that scenario

7 has nonzero values for y31 and y32. This scenario has a reliability

of 0.3 for generator 1 and it is impossible to meet the combined

demand of 2700. The side problem is infeasible for this scenario,

but the variables y31 and y32 allow the submodel to have a

feasible but costly solution. We have summed the probabilities

of the feasible scenarios for the Feasible Probability values

below.

Summarizing the solution

we have.

It is interesting

to compare this result with the optimum solution obtained

with GAMS running

on

a workstation. The L-shaped solution is within the specified

tolerance of the optimum. We could find a better solution with

a smaller tolerance, but more iterations of the method would

be necessary.

We compare these solutions with the solutions from several

other strategies below. |

Transportation Model |

| |

For the solutions above, we used the LP form of the transportation

model. The side model construction does not work when the master

problem is a transportation model. We can use the transportation

model, together with the random variables add-in, to find

solutions that recognize the stochastic nature of the situation.

We construct the transportation model using

the Math

Programming add-in. In the figure below, the range

enclosed by the bold outline is the original model. The information

outside the outline relates the stochastic problem to parameters

of the transportation model. The worksheet also includes

information not pictured.

This is

described

later.

The maximum supply in the range H11:H13 and the minimum demand

in the range D14:F14 are controlled by the first-stage decisions

and the values of the random variables. The figure shows one

sample point for the random variables and one solution for

the first-stage decisions. We show representative equations

on the figure. We illustrate the computation with x =

(2000,1000). These values are in K11 and K12. |

| |

| |

The values of generator capacities are in cells

K11 and K12. The values of the reliabilities are in cells

M11 and M12. These are transferred by equation from cells

D27 and E27. The products of the capacities and reliabilities

determine the upper bounds on shipments in cells H11 and

H12. The upper bound for subcontracting is set to a high

value so that it is not limiting. The demands are placed

as lower bounds to shipments in cells D14, E14 and F14. These

values are transferred by equations from cells F27, G27 and

H27. The cost of the solution has two parts. The installation

cost is computed in cell L14, and the operating cost transferred

from F4 to L15. The total cost is in L16. In L17 we place

a logical expression that computes to FALSE when the amount

shipped from the Subcontractor is greater than 0. The transportation

model has a feasible solution for all x,

but the generator capacities are feasible only when no subcontractor

shipments are necessary.

At the bottom of the worksheet we see cells

that are not part of the transportation model, but are used

to

specify values for the random variables. Row 26 has index

values that range from 1 to 3. Row 27 has the corresponding

values of the random variables taken from the table in rows

29 through 31. The index values are provided by the enumeration

form described below.

|

The Expected Cost |

| |

For a given x, we compute

the expected value of the recourse problem. We use the Functions feature

of the Random Variables add-in

for this purpose. Read the linked sections for the details.

To create a form choose Function from

the add-in menu to display the dialog below. Use 5 as the number

of random variables and 2 as the number of functions. The probability

values are given by User distributions.

The word Network identifies the Jensen

Network Solver to be used to solve the transportation

model. |

| |

|

| |

The form is constructed as below. For the example,

we have placed it immediately to the right of the transportation

model. The five distributions are at the top of the form. Rows

16 through 24 are used by the enumeration process. Rows 25

through 33 define the functions to be evaluated and the results.

This form is set to find the expected cost and the probability

that the given value of x results in a feasible

solution.

To find the expected value of the transportation

solution we enumerate all possible values for the random variables.

Since each random variable has three values there are 3 to

the fifth power, or 243, combinations. This is accomplished

by selecting the Moments command

from the menu. The program runs through all combinations of

the random variables. The values for each combination are placed

on the transportation model and the model is solved with the Network add-in.

The Random Variables add-in then combines all these

results to find the expected cost and the probability of a

feasible solution. These are in Q32 and R28 respectively. |

| |

|

| |

For the example we have:

|

| |

The same process is used to compute several other solutions

below. For each we place the values of x in

cells K11 and K12. Then we choose Moments from the

menu to compute the expected value. |

Expected Value Strategy |

| |

For this solution, we replace the random variables with

their expected values. The model then becomes a deterministic

linear program. The expected values of the random variables

are computed with the usual formulas for discrete random

variables.

Expected Value Model

|

The expected value solution places capacity only at generator

2. The expected cost and feasibility probability are computed

with the Moments command.

|

Scenario Analysis

Strategy |

| |

For this strategy we solve the

problem with a wait-and-see approach

and record the solution vector for each combination of the

random variables. This involves the solution of 243 separate

transportation models. We then combine the solutions by weighing

each solution by the probability of the combination and summing

the results. That solution is then used for the first-stage

decisions.

|

Summary |

| |

Comparing the three solutions on this page we note that the

optimum solution and the nearly optimum L-Shaped solution

dominate the other two in that it has a smaller cost and a

greater probability

of

feasibility.

Solution |

Objective Value |

Feasibility Probability |

| Optimum Solution |

1,927,687 |

0.902 |

| L-Shaped Algorithm Solution |

1,927,689 |

0.902 |

| Expected Value Strategy |

2,433,951 |

0.700 |

| Scenario Analysis Strategy |

2,629,301 |

0.466 |

|

| |

|