|

|

|

Stochastic

Programming |

|

-

Simple Recourse Example: Product Mix |

|

This example was borrowed from An Optimization Primer,

An Introduction to Linear, Nonlinear, Large Scale, Stochastic

Programming and Variational Analysis, by Roger J-B Wets,

January 11, 2005 (unpublished manuscript).

Consider a product mix problem. A furniture maker makes

four products: P1, P2, P3 and P4. Two manufacturing resources

are required: carpentry and finishing. The requirements

measured in hours per unit are known and shown in the table

below along with the profit per unit of product.

Product Parameters |

P1 |

P2 |

P3 |

P4 |

Carpentry Hours per

Unit |

4 |

9 |

7 |

10 |

Finishing Hours per

Unit |

3 |

1 |

3 |

4 |

Profit per Unit |

15 |

25 |

21 |

31 |

Our problem is to select the product mix to maximize total

profit, but the availability of the resources are not known.

Rather we have four equally likely estimates of the hours available

for each resource. The random variables that determine the

resource availabilities are independent.

Resource Distribution |

1 |

2 |

3 |

4 |

Carpentry Hours Available |

4800 |

5500 |

6050 |

6150 |

Finishing Hours Available |

3936 |

3984 |

4016 |

4064 |

Probability |

0.25 |

0.25 |

0.25 |

0.25 |

The mix chosen will require some number of hours for the resources.

This is called a decision making with recourse. We must chose

the mix before the uncertain quantities are known. Once the

uncertainty is realized we must make additional decisions,

called the recourse decisions, to adjust for the new conditions.

We use the notation below to describe the model with accuracy.

|

Expected Value Solution |

| |

The example problem is a product mix problem

with only four products and two resources. The problem has

four products with production amounts as x1 through x4.

The unit profits for the products are in the objective coefficient

row. The problem has two resources, carpentry and finishing.

The hours used for the products on the resources are shown

in the constraint matrix. The available hours for the resources

are uncertain. For the expected value solution we use the expected

resource availabilities as the RHS values.

The optimum mix includes P1 and P2. The solution uses all

available carpentry and finishing hours.

As illustrated previously, the expected value solution

is not very acceptable because there is a good chance that it

will not be feasible once the amount of resource availability

is revealed. In this case there is a 50% chance that there will

a shortage in carpentry hours and a 50% chance that there is

a shortage of finishing hours. Since the random variables are

independent, the probability that the solution is feasible is

only 25%.

Resources |

Used |

1 |

2 |

3 |

4 |

Carpentry Hours |

5625 |

4800 |

5500 |

6050 |

6150 |

Finishing Hours |

4000 |

3936 |

3984 |

4016 |

4064 |

Probability |

|

0.25 |

0.25 |

0.25 |

0.25 |

|

Recourse Costs |

| |

To model the problem with simple

resource, we prescribe costs for exceeding the resource

amounts available. These are the shortage costs. They might

represent the cost of paying workers overtime pay. We also

prescribe the costs for falling below the amounts available.

These are the overage costs. They might represent the cost

associated with idle workers.

For this example, the number of hours available for the

resources happens to be less than the amount used by the production

plan, there is a shortage of hours and extra hours must be

purchased to make up the shortage. The cost of extra carpentry

hours is $5 per hour and the cost of extra hours for finishing

is $10 per hour. There is no penalty for when the available

hours exceeds the amount used (overage). The costs are shown

in the table below.

Penalties |

|

|

Carpentry |

5 |

0 |

Finishing |

10 |

0 |

For the expected value solution, the penalties and their costs

are computed on the left below. The associated formulas are

on the right.

Although the profit of the expected value solution is 20761,

it must be reduced by the expected cost of hiring extra hours

for the resources. This reduces the expected profit

to 19373. The simple recourse model explicitly considers the

recourse costs, so a better solution should be available. |

Simple Recourse |

| |

To express the simple recourse

problem with a mathematical programming model, we rewrite the

constraints to explicitly determine the amounts of each resource

used and the objective to include the recourse costs. The objective

is written as a maximization to reflect the goal of the example

to maximize profit less the expected recourse costs.

For discrete distributions the expected recourse cost is a

piecewise linear function of  .

The calculation on the left shows the implementation of the

expressions on the right. The important information for the

math programming model are the piecewise costs and upper bounds

for each piece. .

The calculation on the left shows the implementation of the

expressions on the right. The important information for the

math programming model are the piecewise costs and upper bounds

for each piece.

It is an important result that the piecewise costs increase

as the index increases. Thus we have:

The expected cost is therefore a convex function of .

For example the expected cost for the carpentry resource is

shown below. Concavity assures that the result of the optimization

is a global optimum.

The Math programming model for the simple recourse

problem is below. Two constraints represent the resource requirements

and two provide the piecewise linear expected recourse cost.

The optimum solution produces more P3

than the expected value solution. |

|

| |

The solution still has a 50% chance of using

all the carpentry hours available, but exactly 6050 hours are

used. This is one of the realizations of the discrete probability

distribution. The solution uses the smallest possible value

of the finishing hours available, so no extra hours are necessary.

Resources |

Used |

1 |

2 |

3 |

4 |

Carpentry Hours |

6050 |

4800 |

5500 |

6050 |

6150 |

Finishing Hours |

3936 |

3936 |

3984 |

4016 |

4064 |

Probability |

|

0.25 |

0.25 |

0.25 |

0.25 |

|

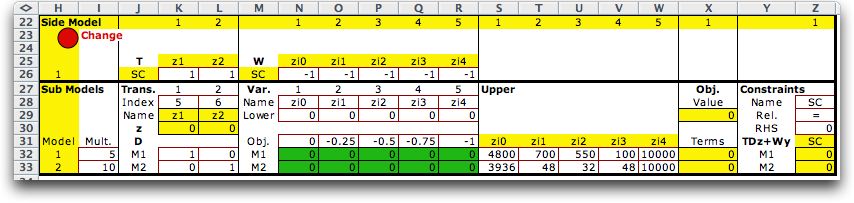

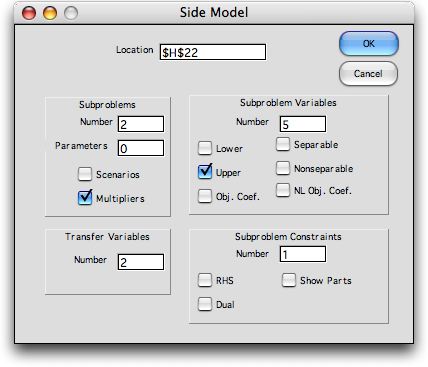

Side Model |

| |

This small problem is easily setup using the

model structure provided by the Math Programming add-in, but

the piecewise linear portion increases the extent of the A matrix.

The side model feature makes

a model that will be more efficient for larger problems with

more values for the discrete random variables. For the example

problem, we first constraint a linear programming model that

includes the variables z1 and z2, but not the

variables associated with the piecewise linear approximation.

We then choose the Side command from

the Math Programming menu and fill in the fields as below.

The side model form is constructed starting in

cell H22. The data for this problem has been filled in, but

the problem has not yet been solved. To

keep the model small we have taken advantage of the fact that

the probability values were the same for each random variable.

The multipliers in column I describe the costs of the extra

hours. The penalties are shown as negative values because we

are maximizing the objective function. The coefficients in the

range (N26:R26) show the coefficients of the piece-wise variables

and the coefficients in the range (S32:W33) show the upper

bounds on the individual pieces. |

|

| |

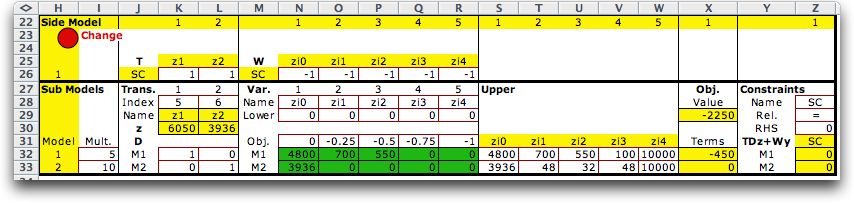

Solving the problem by clicking the Solve button

in the upper left corner of the LP model calls the Excel Solver.

The solution is shown below. The solution is provided in the

green areas of the worksheet. The solution is the same as for

the extended form of the LP. |

| |

|

| |

Although not so obvious for this small problem,

the side

model feature makes

a model that is be more efficient for larger problems with

more values for the discrete random variables. The side model

grows linearly with the number of pieces in the discrete representation

and almost linearly with the number of random RHS values. |

| |

|

|