|

Variable Activities do not have a fixed time, rather

the durations of these activities are determined by the start

and finish times of other activities. They have variable activity

times. To illustrate, consider again the pump installation example.

In addition to the situation described on the Example

and Cash Flow pages, we add some

new features to the project. We realize that a complicated cost

and revenue structure is probably not reasonable for this project

with such a short duration, but the example illustrates this

new modeling capability.

- The company must rent temporary buildings and other equipment

that are to be used for the entire duration of the project.

There is a deposit of $500 and the rent is $10 per hour.

One employee is hired to work in the office at a cost of

$20 per hour. At the end of the project the deposit will

be returned.

- During the process of pouring and curing the slab, special

concrete equipment must be rented. The cost of this equipment

is $10 per hour. These payments begin with activity A and

end with activity D.

- The company must hire a Registered Professional Engineer

for all activities regarding electricity. The requirement

begins with the running of the electrical line (G) and ends

when the motor is tested (K). The cost of the engineer is

$50 per hour. There is an additional paperwork charge of $200

when the engineering is hired.

- The company will outsource the ordering and installation

of the pump unit. The requirement begins with the ordering

of the pump unit (B) and ends when the unit is installed (H).

There is an initial payment of $200 for this service and a

final payment of $300. The crew requirements are reduced to

zero for activities B and H, but one person is allocated to

this variable activity for supervision. The cost of this person

is $20 per hour.

- In order to finance the project the company will take out

a construction loan of $10,000. The money will be received

at the start of the project. The company must return to the

lender $10,500 at the end of the project. We also include

in this activity the management costs for the project of $80

per hour.

These activities are different than those formerly described

in that their starting times and ending times depend on the

start and end times of other activities and are not fixed.

For a variable activity we specify two fixed time activities,

a

From Activity and a To Activity. The activity

described by paragraph 2 above starts at the same time as A

(the From Activity) and ends at the same time as

D (the To Activity) . When the From activity

is left blank, the variable activity starts at the beginning

of the project. When the To

Activity

is left blank the variable activity ends when the project is

completed.

For an additional variation, the company receives

income for the project. The company will be paid $27,000,

to be received in three payments. The first payment of $9,000

will be received at the completion of the slab curing step

(activity D). The second payment of $9,000 will be received

when the electric motor is installed (activity I). The last

payment of $9,000 will be received when the project is completed

(the End

activity). Three variable activities are added to represent

the payments. The variable activities are defined in the table

below.

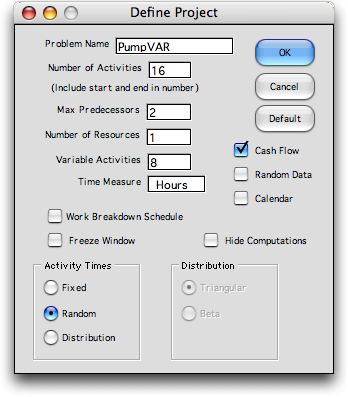

The project is defined

using the dialog below. We enter 8 as the number of Variable

Activities.

The Change

button on the project definition page allows this number to

be increased or decreased.

The data form for the complete problem is shown below. We

have adjusted the cash flow data for some of the activities

to reflect the new information. The crew resources for G and

H have been reduced to 0 because these activities have been

outsourced. The variable activities require some additional

crew resources. Costs are represented as positive

cash flows and revenues are negative. We have associated the payments

with the final cash flows for the activities that determine

the timing of the payments. |

| |

Since the fixed times

have not changed for this example, the critical path and other

time-related results are the same as when variable activities

were not considered. The variable activities do not affect the

early and late schedule, however, they do simplify the modeling

of costs and resources when activities span a series of fixed-time

activities. These will affect the optimum schedule when costs

and resources are considered.

Of course it is important that a variable activity not end

before it begins. This illogical result is possible if one chooses

a From activity that is not restricted by the precedence

relations from starting after the end of the To activity.

The program does not check for this, but in most reasonable

cases the normal relationships between fixed-time activities

will prevent it.

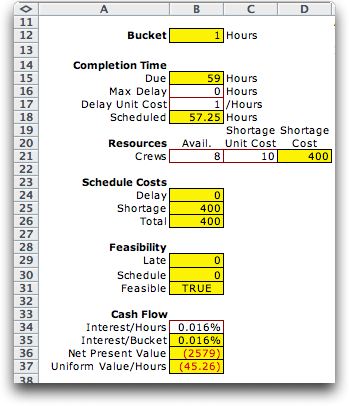

Clicking the Solve button builds the equations that determine

the scheduled start and finish times. The example below shows

some nonzero delays. They are determined during the scheduling

process. The variable activities start and stop based on the From and To activities. |

| |

Clicking the Cash Flow button at the top of the schedule

worksheet computes the cash flow for three schedules: the schedule

with the activities beginning at their Earliest start

times, the schedule currently specified on the worksheet, and

the schedule with the activities beginning at their Latest start

times. The three results are shown in the green field above

the graph. Only the first few buckets are shown and the table

continues to the right.

The cumulative cash flows are shown in a chart as below. The

sudden changes in the cash flow indicates large receipts and

expenditures. The last observations on the right shows the

cumulative cash flows at the end of the project. These are

different for the three cases because the variable activities

have different durations for the cases and hence impose different

cash flows. The current schedule uses delays to reduce the

cost of shortages. The cumulative cost at the end of the time

horizon indicate whether the project makes a profit. The cumulative

cost for the early time schedule is -1340, indicating a profit

of 1340. The profit for the late schedule is 2170, while the

profit for the current schedule is 2580. |